How are rabbi trust distributions taxed?

Ava Robinson

Published Feb 10, 2026

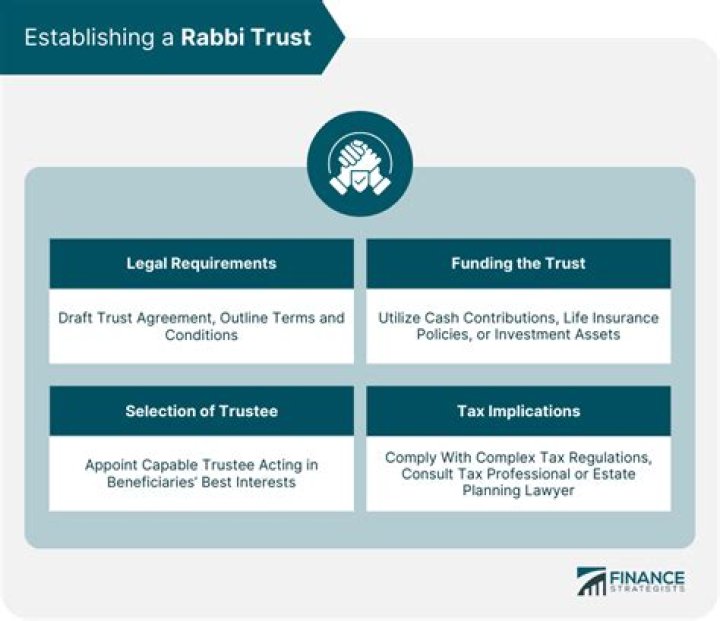

A rabbi trust is considered a grantor trust for income tax purposes, resulting in trust income taxed to the employer. Contributions to the trust are not tax deductible by the employer. However, the employer may deduct the full amount of the benefit payment as the trust makes payments to plan participants.

Are rabbi trusts revocable?

The rabbi trust is usually irrevocable, although it can be designed to be revocable until the happening of certain events such as a change in control.

Are rabbi trusts taxable?

Rabbi trusts allow employees’ assets to grow without them having to pay tax on any gains until they withdraw their money. In this sense, a rabbi trust is similar to a qualified retirement plan. A rabbi trust does not provide any tax benefits for companies that make its use limited compared to other types of trusts.

Can you rollover a rabbi trust?

Distribution rules for Rabbi Trust accounts are not as flexible as the rules for 403(b) accounts. You can’t take early withdrawals, including a loan or hardship, and distributions from the Rabbi Trust can’t be rolled over to another qualified retirement account such as an IRA.

Why is it called a rabbi trust?

A “rabbi trust” is so called because the first such trust was established by a Jewish congregation for its rabbi. The congregation applied for and obtained a private letter ruling (PLR) from the Internal Revenue Service (IRS) which clarified the tax consequences of the establishment of the trust to the rabbi.

Which of the following best describes a rabbi trust?

Which of the following best describes a Rabbi Trust? A Rabbi Trust can only be used by non-profit religious groups (457 plans). A Rabbi Trust provides a funding vehicle that remains available to the creditors of the plan sponsor.

What is an excess benefit plan?

(36) The term “excess benefit plan” means a plan maintained by an employer solely for the purpose of providing benefits for certain employees in excess of the limitations on contributions and benefits imposed by section 415 of title 26 on plans to which that section applies without regard to whether the plan is funded.

Who are beneficiaries of a trust?

A beneficiary of trust is the individual or group of individuals for whom a trust is created. The trust creator or grantor designates beneficiaries and a trustee, who has a fiduciary duty to manage trust assets in the best interests of beneficiaries as outlined in the trust agreement.

How is a funded excess benefit plan different from a qualified plan?

A funded excess benefit plan can provide the benefit of tax deferral only if the employee’s benefit is subject to a substantial risk of forfeiture. In contrast, an unfunded excess benefit plan can provide the benefit of tax deferral even if the employee’s benefit is fully vested.

Can a deferred bonus be transferred to a rabbi trust?

The rule does not apply to assets located in a foreign jurisdiction if substantially all of the services to which the deferred compensation relates are performed in that jurisdiction. This provision also limits the use of rabbi trusts in instances where assets are transferred to a rabbi trust upon a change in the employer’s financial health.

How much Nil Rate Band is available to second Trust?

This means that only £162,500 of the nil rate band is available to the second trust (full nil rate band of £325,000 less previous CLT of £162,500 = £162,500). As this CLT is £200,000, the surplus over the £162,500 (£37,500) will be subject to an entry charge of 20%.

How does the Charitable Remainder Trust ( CRUT ) work?

The Charitable Remainder Unitrust or CRUT pays an income stream to the taxpayer that is based on a taxpayer chosen percentage of the fair market value of the CRUT-owned assets every year.

What’s the maximum term of a charitable trust?

The maximum term allowed on this type of trust is 20 years, which effectively means that after the 20-year period has ended, the trust must pay out the balance to the charitable beneficiary, which may either be a public charity or a private foundation.