How are K-1 profits taxed?

Andrew Mclaughlin

Published Apr 05, 2026

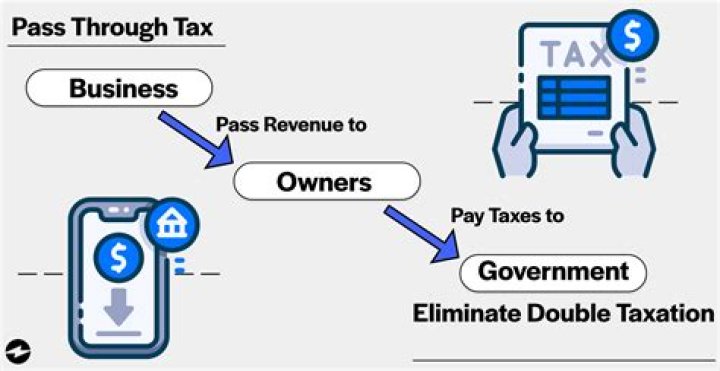

A partnership is not subject to federal income tax. Rather, its owners are subject to Federal income tax on their share of the profit. Schedule K-1 is then used to show each partner’s allocated share of the various types of income and deductions.

Like sole proprietorships, partnerships are “pass through” entities. A partnership is not subject to federal income tax. Rather, its owners are subject to Federal income tax on their share of the profit. Schedule K-1 is then used to show each partner’s allocated share of the various types of income and deductions.

Do we pay income tax on money already taxed?

The IRS loves to tax money twice and you’re probably paying tax on money that was already taxed, as well. We’re talking about dividends, inheritance and a host of other “gotchas” implemented by the IRS so they can grab and grab again. Dividends are those checks you receive from stocks you own.

What makes K1 tax form different from other tax forms?

Schedule K1 Form 1065 is used to report one’s share of a partnership. Income Tax Return for an S Corporation (Form 1120S). Schedule K1 Form 1120S is used to report one’s share of a corporation. What Makes K1 Tax Form Different?

Do you have to file a Schedule K-1?

Schedule K-1 of Form 1041, which must be filed by beneficiaries of trusts or estates Schedule K-1 of Form 1120S, which must be filed by the owners of S corporations Although these forms are similar, in this guide we’ll focus exclusively on Schedule K-1 of Form 1065, to be filed by partnerships.

Do you have to pay taxes on withdrawals on a K-1?

Although withdrawals and distributions are noted on the K-1, they generally aren’t considered to be taxable income. Partners are taxed on the net income a partnership earns regardless of whether or not the income is distributed.

How does an LLC K-1 affect my taxes?

An owner’s K-1 form shows his LLC income for the year, like a W-2 does for a salaried position. The owners of an LLC can choose to have the IRS treat the company as a corporation, a partnership or a disregarded entity: As a partnership, profits are allotted among the members at the end of each year.