Does Titlemax report to credit bureaus?

Henry Morales

Published Feb 10, 2026

In most cases, a title loan won’t have any impact on your credit scores. That can be good and bad. For starters, most title lenders don’t run a credit check when you apply. On the flip side, title lenders don’t report your payments to the credit bureaus, which means a title loan won’t help your credit scores either.

Is my title loan tax deductible?

The interest on a car title loan is not generally tax deductible; however, LoanMart has competitive interest rates and long repayment terms, so you can pay off your loan FAST which can be a much better benefit. The faster you pay off your car title loan, the less you will pay in interest.

How to pay off a title loan fast?

Wondering how to pay off a title loan fast is good, but before you can do this, you must be approved for the loan. The main requirement for approval of a car title loan with TitleMax® is that you own a car that’s paid off. You must hold the lien-free title to the car. The title must have your name on it as the owner.

How to calculate the interest rate on a title loan?

To calculate any loan accurately you will need the right interest rate. It is important to compare loans using the same interest rate term. If you have the Annual Percentage Rate (APR) you need to compare it to APR; and if you have a Monthly Rate you need to compare to another Monthly Rate.

Are there any fees with a title loan?

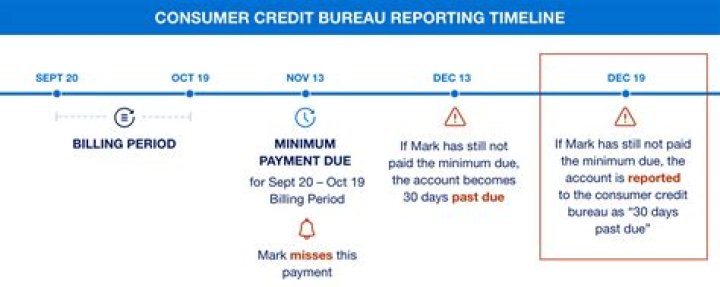

Title loan providers might charge other fees associated with taking out and repaying the loan, including: Lien filing fees. Your lender might ask you to cover the cost of putting a lien on your vehicle’s title. Late payment fees. If you’re late on a payment, you could face a fee equal to 5% of the payment due, though it varies by lender.

What do you need to get a title loan?

The main requirement for approval of a car title loan with TitleMax® is that you own a car that’s paid off. You must hold the lien-free title to the car. The title must have your name on it as the owner.