Does the IRS audit partnerships?

Henry Morales

Published Apr 12, 2026

In 2021 the IRS plans to begin an initiative to audit large partnerships using the powerful centralized partnership audit tools Congress gave the agency when it enacted the Bipartisan Budget Act of 2015 (BBA).

What does the IRS consider a partnership?

A partnership is the relationship between two or more people to do trade or business. Each person contributes money, property, labor or skill, and shares in the profits and losses of the business.

Can the partnership representative be an entity?

A partnership may designate any person, an entity or itself as a PR, but they are required to have a substantial presence in the United States. If an entity is designated as a PR: the partnership must also appoint a designated individual to act on the entity’s behalf.

How do you audit a partnership?

An Auditor should carefully read the partnership deed and note down all the important provisions regarding;

- Nature of business.

- Profit sharing Ratio.

- Interest on capital and drawings.

- Loans and drawings.

- Borrowing power of partner.

- Salary and remuneration.

- Capital of the partner.

- Restriction on the rights of a partner.

What is an LLC partnership representative?

Most multi-member LLCs are taxed as partnerships and must comply with the federal tax rules that apply to partnerships. These rules require the LLC to designate someone—called a partnership representative in the tax law—to represent the LLC before the IRS in an audit.

Does tax matters partner still exist?

One change is that there is no longer a “tax matters partner” (also referred to as a tax matters member) which you will see in most operating agreements (at least for multi-member LLCs classified as partnerships for tax purposes—our working assumption for purposes of this post).

Does partnership need to be audited?

All enterprises (sole proprietors) or partnership are NOT required by Business Registration Act to appoint auditors to audit their accounts.

Why are there new rules for partnership audits?

The new partnership audit rules are designed to make it easier for the IRS to examine partnerships and collect any resulting underpayments through the use of centralized proceedings. Under the previous partnership audit rules, the audit, assessment and collection of tax was complex and administratively burdensome on the IRS.

How to designate a partnership representative to the IRS?

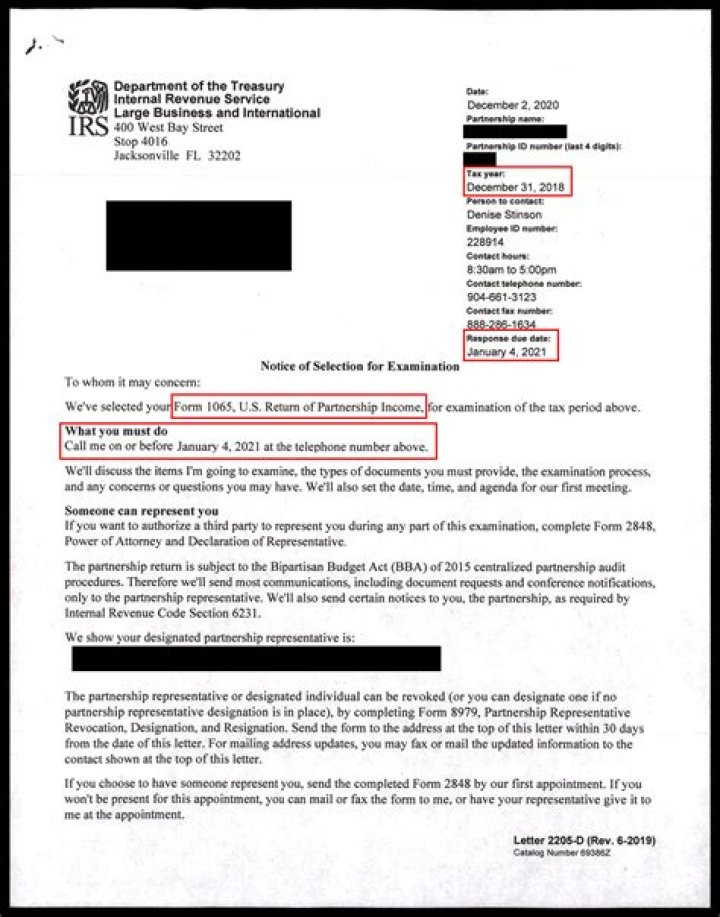

Never mail separately or fax (by itself, as a stand-alone filing) to the IRS — Form 8979, Partnership Representative Revocation, Designation, and Resignation. (2) directly to the current IRS employee point of contact after the issuance of either Letter 2205-D or Letter 5893.

Are there any changes to the partnership tax rules?

IRS has recently enacted partnership tax changes which may have a significant impact on you. These changes, commonly referred to as the “partnership audit rules”, are expected to dramatically increase the IRS audit rates for partnerships and will require partners to carefully review, if not revise, their partnership’s operating agreement now.

Who is the partnership representative under the BBA?

The partnership and the partners are bound by the actions of the partnership representative under the BBA. The partnership representative is comparable to the Tax Matters Partner under the Tax Equity and Fiscal Responsibility Act of 1982 (TEFRA) but has more authority.