Does state matter for 529 plan?

Henry Morales

Published Mar 05, 2026

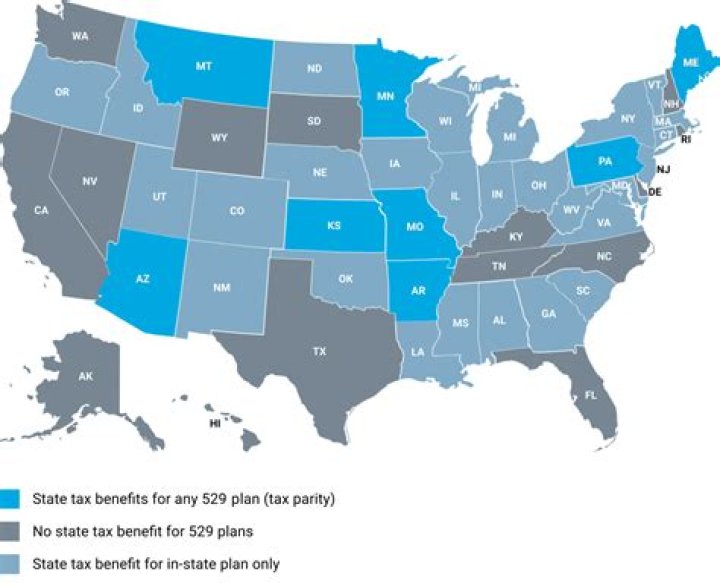

Questions about Moving to a Different State You can use a 529 plan from any state to pay for an eligible college in any state. State income tax breaks are generally limited to the 529 plan for the state of residence, although seven states provide their state income tax breaks for contributions to any state’s plan.

Are 529 plans state or federal?

529 education savings plans — tax-advantaged accounts that are designed to help families save for educational expenses — are authorized by the federal tax code but administered at the state level. Therefore, state policy is a key factor in how these plans function.

Are there any tax benefits to a 529 plan?

529 plans offer unsurpassed income tax breaks. Although contributions are not deductible, earnings in a 529 plan grow federal tax-free and will not be taxed when the money is taken out to pay for college.

Are there any state tax benefits for 529 plan?

The most common benefit offered is a state income tax deduction for 529 plan contributions. However, Indiana, Utah and Vermont offer a state income tax credit for 529 plan contributions and Minnesota offers a state income tax deduction or tax credit, depending on the taxpayer’s adjusted gross income. Limits on annual 529 state income tax benefits.

How to make the most of your 529 plan?

Here are three tips to help you make the most of your 529: 1. Don’t be blinded by the tax break; select a plan based on performance, low costs and fund choice, not state tax breaks. Any state plan you invest in allows you to accrue income and capital gains tax-free.

How much can you contribute to a 529 plan in Ohio?

Ohio offers married taxpayers a state tax deduction for 529 plan contributions of up to $4,000 per year for each beneficiary Married grandparents in Nebraska who want to contribute $15,000 toward college savings for five grandchildren would only be able to deduct $10,000 from state taxable income.

Who is the owner of a 529 savings plan?

Anyone can open and fund a 529 savings plan—the student, parents, grandparents, or other friends and relatives. Unlike a custodial account that eventually transfers ownership to the child, with a 529 savings plan, the account owner (not the child) calls the shots on how and when to spend the money.