Does self-employed income include expenses?

Ava Robinson

Published Apr 04, 2026

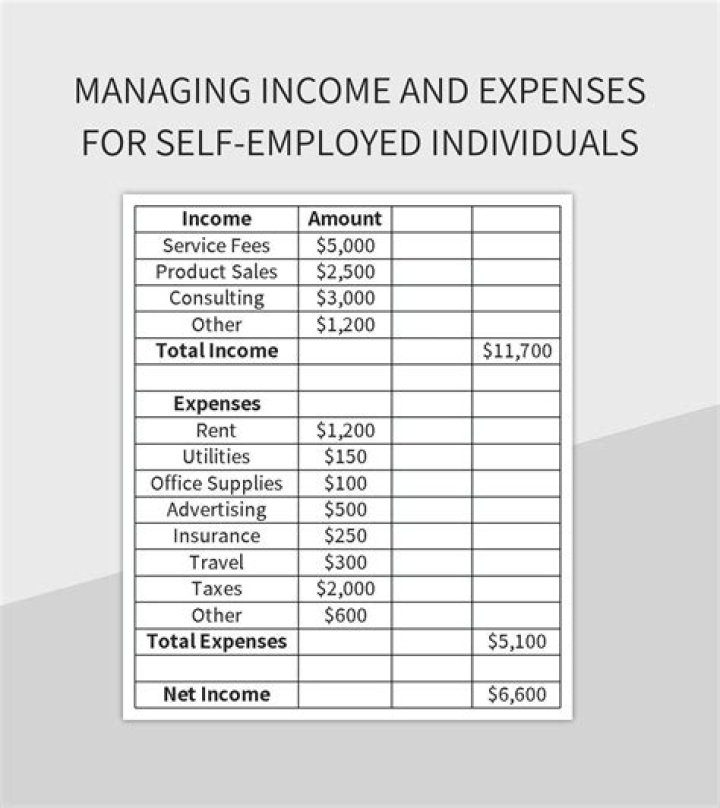

Self-employed persons are taxed on their net self-employment income—what’s left over after they enter their earnings and deduct their qualifying business expenses on Schedule C, “Profit or Loss From Business.” Business expenses that can be deducted on Schedule C directly against income include expenses for: Advertising.

What is self-employment income and expenses?

Self-employed individuals generally must pay self-employment tax (SE tax) as well as income tax. You do this by subtracting your business expenses from your business income. If your expenses are less than your income, the difference is net profit and becomes part of your income on page 1 of Form 1040 or 1040-SR.

What is included in self-employment income?

Self-employment income is earned from carrying on a “trade or business” as a sole proprietor, an independent contractor, or some form of partnership. To be considered a trade or business, an activity does not necessarily have to be profitable, and you do not have to work at it full time, but profit must be your motive.

How do I report self employment expenses?

Self-employed taxpayers must file a Schedule C, Profit or Loss from Business, or Schedule C-EZ, Net Profit from Business, with their Form 1040. For expenses less than $5,000, use Schedule C-EZ.

Can clergy deduct half of self employment tax?

Easy-to-miss deductions for ministers The self-employment tax deduction—You can deduct half of your self-employment tax on Form 1040 as an adjustment to income.

What kind of taxes do clergy pay on self employment?

Housing and utility allowances are, however, subject to self-employment taxes (Social Security and Medicare). How is Your Tax Return Different from Everyone Else’s? Members of the clergy have unique tax situations.

Can a self employed minister claim a tax deduction?

If a self-employed minister’s compensation includes a parsonage or housing allowance which is exempt from income tax, the prorated portion of the expenses allocable to the tax exempt income is not deductible.

Is the clergy housing allowance excluded from income?

A housing allowance is a portion of clergy income that may be excluded from income for federal income tax purposes (W-2 “Box 1” wages) under Section 107 of the Internal Revenue Code. To

Where can I find a clergy tax preparation guide?

(Federal Reporting Requirements Guide)as references to help clergy, treasurers and bookkeepers, and tax preparers in better understanding clergy taxes. These guides are available on CPG’s website at cpg.org.