Does FIRPTA apply to foreign corporations?

Andrew Mclaughlin

Published Mar 29, 2026

FIRPTA applies to foreign corporations, partnerships and other entities selling U.S. real properties. Under FIRPTA, when a foreign investor is selling a real estate property, the buyer or its agent is required to withhold 15% of the amount on the disposition.

Are corporations subject to FIRPTA?

FIRPTA authorized the United States to tax foreign persons on dispositions of U.S. real property interests. For cases in which a U.S. business entity such as a corporation or partnership disposes of a U.S. real property interest, the business entity itself is the withholding agent.

Which document is one of the most critical to closing?

The Deed: public record of the ownership of the property It often includes a description of the property and signed by both parties. Deeds are the most important documents in your closing package because they contain the statement that the seller transfers all rights and stakes in the property to the buyer.

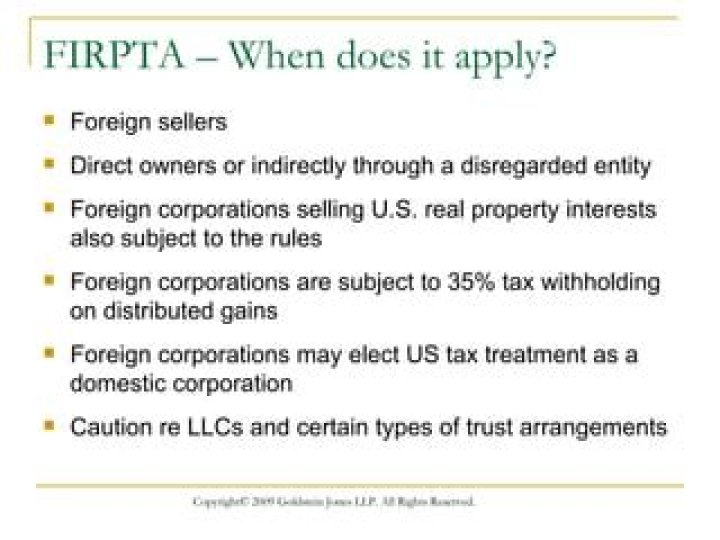

FIRPTA applies to foreign corporations, partnerships and other entities selling U.S. real properties. It also applies to individual sellers who are considered non-residents. The amount of any liability assumed by the transferee or to which the property is subject immediately before and after the transfer.

Can a foreign corporation be a Usrphc?

Although a foreign or domestic corporation can be a USRPHC, the implications are generally different. If a domestic corporation is a USRPHC or was one within the 5 years preceding the disposition and the cleansing rule does not apply, its stock is a USRPI (IRC 897(c) (1)(A)(ii)). See IRC 897(c)(5).

Can a foreign seller be exempt from FIRPTA withholding?

Since we know that the IRS implements a FIRPTA Withholding on foreign sellers, we can use their list of FIRPTA exceptions to decide if an exemption exists. According to the IRS, you can be exempt from FIRPTA withholding if you meet one or more of the following:

Can a foreign trust be subject to FIRPTA?

U.S. trusts are not subject to the FIRPTA withholding rules. Foreign trusts on the other hand are subject to the FIRPTA withholding rules in connection with the sale of the trust’s real property. Internal Revenue Code Section 7701 (a) (30) (E) contains a two-part test for determining whether a trust is a U.S. or foreign trust.

Can a domestic corporation be taxed Under FIRPTA?

Domestic corporations are not subject to the withholding rules under FIRPTA, so withholding will not be required in cases where entities otherwise subject to withholding have elected to be taxed as a domestic corporation.

When does FIRPTA require a determination to be made?

FIRPTA requires a determination to be made if the seller of property is a U.S. person or a foreign person. This is because FIRPTA imposes a withholding obligation on the seller of real estate. If the seller of real property is a foreign person and not a “U.S. person” (as defined by the Internal Revenue Code), FIRPTA withholding may be required.