Does beta measure systematic or unsystematic risk?

Mia Ramsey

Published Feb 15, 2026

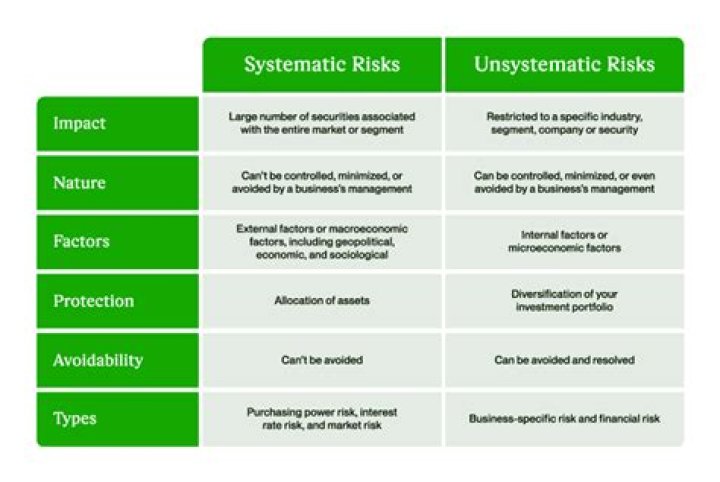

Beta is a measure of the volatility—or systematic risk—of a security or portfolio compared to the market as a whole. Beta is used in the capital asset pricing model (CAPM), which describes the relationship between systematic risk and expected return for assets (usually stocks).

What does a beta of 1.0 mean?

A beta of 1.0 means that for every 1% change in the market, an individual security or investment will likely move 1%. In other words, it tracks directly with the market. Stocks with betas greater than 1.0 have more amplified movements than the market itself; they have a greater level of risk.

What does it mean when beta is 1?

A beta of 1 indicates that the security’s price tends to move with the market. A beta greater than 1 indicates that the security’s price tends to be more volatile than the market. A beta of less than 1 means it tends to be less volatile than the market. This means it is two times as volatile as the overall market.

What is the measure of beta?

Beta is a measure of a stock’s volatility in relation to the overall market. By definition, the market, such as the S&P 500 Index, has a beta of 1.0, and individual stocks are ranked according to how much they deviate from the market. A stock that swings more than the market over time has a beta above 1.0.

Does higher beta mean more systematic risk?

The beta of a stock or portfolio will tell you how sensitive your holdings are to systematic risk, where the broad market itself always has a beta of 1.0. High betas indicate greater sensitivity to systematic risk, which can lead to more volatile price swings in your portfolio, but which can be hedged somewhat.

How do you calculate beta systematic risk?

Beta could be calculated by first dividing the security’s standard deviation of returns by the benchmark’s standard deviation of returns. The resulting value is multiplied by the correlation of the security’s returns and the benchmark’s returns.

What does a beta of 1.5 indicate?

A beta of 1.5 means that a stock’s excess return is expected to move 1.5 times the market excess returns. E.g., if market excess return is 10%, then we expect, on average, the stock return to be 15%.

Why is beta a measure of systematic risk?

Beta is the standard CAPM measure of systematic risk. It gauges the tendency of the return of a security to move in parallel with the return of the stock market as a whole. One way to think of beta is as a gauge of a security’s volatility relative to the market’s volatility.

Which is more riskier beta or 1.2 Why?

If a stock moves less than the market, the stock’s beta is less than 1.0. High-beta stocks are supposed to be riskier but provide a potential for higher returns while low-beta stocks pose less risk but also lower returns. If a stock’s beta is 1.2, it’s theoretically 20% more volatile than the market.

How do you calculate unlevered beta?

Formula for Unlevered Beta Unlevered beta or asset beta can be found by removing the debt effect from the levered beta. The debt effect can be calculated by multiplying debt to equity ratio with (1-tax) and adding 1 to that value. Dividing levered beta with this debt effect will give you unlevered beta.