Does a merchandiser prepare a production budget?

Emma Jordan

Published Feb 15, 2026

Budgeting in merchandising companies Budget preparation for merchandising companies and service companies is similar to budgeting for manufacturing companies. A service or merchandising company will not have a production budget or direct material budget and may not have a direct labor or overhead budget.

What is preparation of production budget?

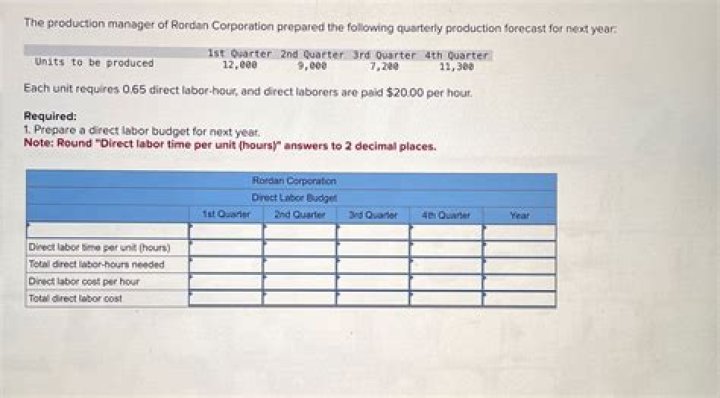

To prepare a production budget, we get the number of goods that the company expects to sell in a given period. Then, subtract any units the company already has in inventory. Remember, inventory means completed but not yet sold to customers. That gives the net number of units that need to be produced that quarter.

Who prepare the production budget?

The production budget, used by businesses that produce products instead of services, is one part of a firm’s operating budget, and is typically developed after the sales budget. The sales budget drives the production budget because it budgets for the forecasted future sales of the firm’s products.

What is the starting point of preparing a production budget?

The first step in the direct materials budget is to convert units of finished goods produced into direct materials needed to produce them by multiplying the number of units produced by the direct materials required to produce one unit of finished goods.

What is material budget?

The materials budget (or materials purchases budget) is used to plan how much raw materials we need to have available to meet budgeted production. This budget is prepare similarly to the production budget as the company must decide how much raw materials inventory they want to have on hand at the end of each quarter.

Which budget is used by merchandising companies?

In a merchandising company, the production budget and the three manufacturing budgets—direct materials, direct labor, and manufacturing overhead—are replaced with the merchandise purchases budget.

How do you prepare a purchases budget?

The budget is created using a simple formula: the desired ending inventory, plus the cost of goods sold, minus the value of the beginning inventory. This equation gives you the total purchases budget.

What budgets are prepared before the production budget?

The direct materials budget is typically prepared before the production budget. A self-imposed budget is a budget that is prepared with the full cooperation and participation of managers at all levels. The sales budget often includes a schedule of expected cash collections.

How do you prepare a merchandise purchases budget?

Inventory to be purchased equals the budgeted ending inventory plus the budgeted cost of sales for the period minus the budgeted beginning inventory. Like most other budgets, the merchandise purchases budget relies on the estimated sales for the period and can’t be made until the sales budget is finished.

What does a production budget include?

The production budget calculates the number of units of products that must be manufactured, and is derived from a combination of the sales forecast and the planned amount of finished goods inventory to have on hand (usually as safety stock to cover for unexpected increases in demand).

How do you prepare a sales budget and production budget?

The sales budget and the production budget involve simple calculations. For example, the company expects to sell 10,000 units of products over the next year. The sales budget then multiplies the number of units by the price of one unit.

What does not appear on selling and administrative expense budget?

1. the quantity of direct materials to be purchased. 2. the cost of direct materials to be purchased. Which of the following expenses would not appear on a selling and administrative expense budget?

When does top management notice a variation from budget?

Top management notices a variation from budget and an investigation of the difference reveals that the department manager could not be expected to have controlled the variation. Which of the following statements is applicable?

Who is held accountable for variances in a budget?

Department managers should be held accountable for all variances from budgets for their departments. b. Department managers should only be held accountable for controllable variances for their departments. c. Department managers should be credited for favorable variances even if they are beyond their control.

Which is not follow from the adoption of a budget?

Which of the following items does not follow from the adoption of a budget? a. Promote efficiency b. Deterrent to waste d. Guarantee of accomplishing the profit objective d. Guarantee of accomplishing the profit objective Which is true of budgets? a. They are voted on and approved by stockholders.