Does 1231 gain include 1250 gain?

John Thompson

Published Apr 02, 2026

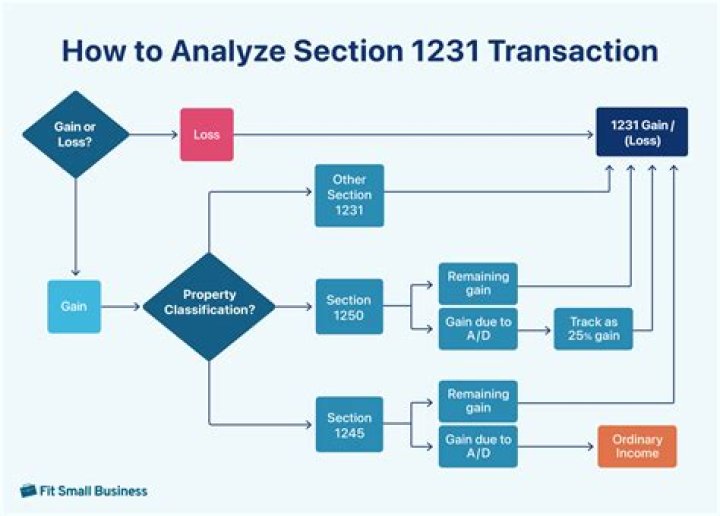

Any remaining gain in excess of both the Section 1250 depreciation recapture and unrecaptured Section 1250 gains will be treated as Section 1231 gain (long term capital gain), which will be taxed at a maximum rate of 15%, through December 31, 2012. The Section 1250 recapture provisions only apply to gains, not losses.

Are Section 1231 gains taxable?

A section 1231 gain from the sale of a property is taxed at the lower capital gains tax rate versus the rate for ordinary income. If the sold property was held for less than one year, the 1231 gain does not apply.

Does 1250 gain capital gains?

Since the unrecaptured section 1250 gains are considered a form of capital gains, they can be offset by capital losses.

Is Land 1250 or 1231 property?

Commercial real estate, residential investment properties, buildings and land used for business are all section 1231 properties. Section 1250 of the Internal Revenue Code deals with depreciation on section 1231 property.

Where do I report section 1231 gain?

Section 1231 gains are given long term capital gain treatment and subsequently reported on Schedule D. So prior year 1231 losses are therefore shown on the Form 4797 to offset current year income and reduce the amount of capital gain.

What is net section 1231 gain loss?

The Section 1231 Tax Advantage A net section 1231 gain is taxed at the lower capital gain rates. A net section 1231 loss is fully deductible as an ordinary loss. In contrast, a capital loss is only deductible up $3,000 in any tax year and any excess over $3,000 must be carried over to the next year.

How are capital gains treated in Section 1231?

Section 1231 recovery (5-yr lookback) and Depreciation recapture on Section 1245 is treated as ordinary income. In contrast, 25% unrecaptured 1250 gain is considered capital gain income. While the rates and resulting taxes can be the same, only capital gain income can offset capital losses.

What’s the difference between Section 1245 and 1250?

Section 1231 is the umbrella for assets belonging to section 1245 and section 1250, and the latter is what determines the tax rate of depreciation recapture. Section 1250 relates only to real property, such as buildings and land.

How are capital gains taxed under Section 1250?

While the gains attributed to accumulated depreciation are taxed at the section 1250 recapture tax rate, any remaining gains are only subject to the long-term capital gains rate of 15%.

Which is an example of an unrecaptured Section 1250 Gain?

Example of Unrecaptured Section 1250 Gains If a property was initially purchased for $150,000, and the owner claims depreciation of $30,000, the adjusted cost basis for the property is considered to be $120,000. If the property is subsequently sold for $185,000, the owner has recognized an overall gain of $65,000 over the adjusted cost basis.