Do you have to pay taxes on a boat as a business?

John Thompson

Published Feb 23, 2026

Once you have established the boat or airplane as a business asset, any personal use becomes a benefit to you personally, and, yes, you must pay taxes on this personal use. Boat or airplane as a business vs. a hobby.

What happens if I put my boat into a corporation?

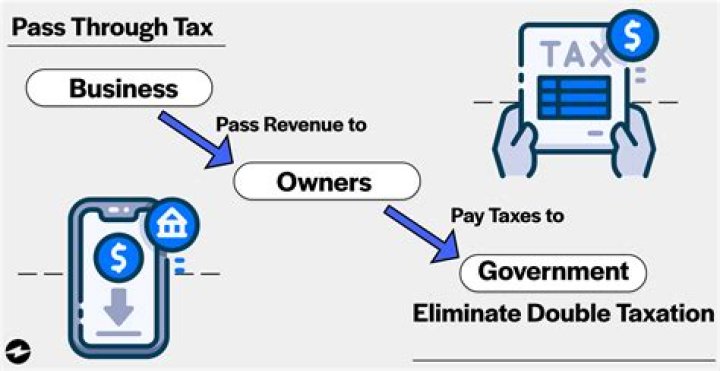

Both an LLC and a corporation provide personal liability protection, which is ostensibly the main goal of putting your boat into a corporate environment. Both LLC’s and Subchapter S Corporations provide pass-through taxation – meaning you would report profits and losses on your personal tax returns.

What do you need to know about buying a boat for business?

If you buy a boat or airplane for business use, you must be able to show that you are running a legitimate business, and are not just taking out fishing or flight charters as a hobby. To avoid IRS scrutiny under “hobby loss” rules, you must keep good business records, show that you intend to make a profit, and make a profit.

Can a boat be considered a business asset?

Now here’s the catch. If you can demonstrate that your boat is a business asset that is used over 50% of the time for business, you must pay taxes on any personal use. Personal use of the boat, which is a business asset, is considered a benefit to you personally.

Can you depreciate a boat as a business asset?

You can depreciate the boat or airplane as a business asset, over its useful life, if it qualifies as a business asset (see below). Expenses. You can deduct expenses for operating the boat or airplane for business purposes. Gasoline, maintenance, mooring fees, insurance, and repairs can be included in the deductible expenses. Document business use.

When to write off a boat or airplane for business purposes?

So, if you use your boat or airplane for charter business purposes, and you also take it out for personal reasons, you must document what percentage of the time you use it for business. To be eligible for depreciated, a listed property must be used predominantly (more than 50 percent) for business purpose. Personal use becomes income.