Do you depreciate investment property under FRS 105?

Ava Robinson

Published Apr 03, 2026

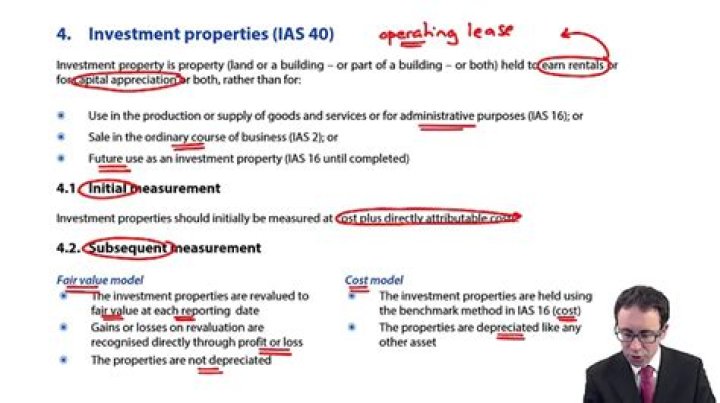

Investment property FRS 105 does not allow the use of revaluations or fair value amounts. This will require the property to be depreciated and tested for impairment at each balance sheet date.

Can investment property companies use FRS 105?

By adopting FRS 105, companies are able to file and prepare abridged accounts and simplify the company’s financial reporting obligations in the following ways: No revaluation at fair value is permitted under FRS 105 meaning investment property could not be revalued to fair value at the end of each financial period.

Is FRS 105 still valid?

FRS 105 is effective for accounting periods beginning on or after 1 January 2016. Early application is permitted. The FRC withdraws the Financial Reporting Standard for Smaller Entities from the effective date of this FRS.

Can group companies use FRS 105?

However, FRS105 cannot be adopted by some types of companies, even where it meets the size criteria, for example, investment companies, financial holding companies and companies that form part of a group that prepares consolidated accounts.

What is the difference between FRS 102 and FRS 105?

FRS 105 is based on FRS 102 but has been adapted to reflect the simpler nature and smaller size of micro-entities and their legal requirements. Differences include: no requirements to account for deferred tax and equity-settled share-based payments; simplified accounting for defined benefit pension schemes; and’

Should I use FRS 102 or FRS 105?

In short, there is no “better” reporting standard for a micro-entity. Under FRS 105, far fewer disclosures are required in the financial statements than under FRS 102 1A. Broadly, under FRS 105, the only disclosures that need be made are in relation to: Advances, credit and guarantees granted to directors.

Can a parent company use FRS 105?

Certain types of entity, such as charitable companies and parent companies that are required or choose to prepare consolidated financial statements, are excluded from the micro-entity regime and therefore cannot apply FRS 105.

Can you change FRS 102 to FRS 105?

As of April 2021, the detailed transition guidance in Transition Guide: FRS 102 and FRS 105 is replaced by Navigate UK GAAP Accounting – Private Company – Framework and statutory requirements – Transition to FRS 102 (Section 35).