Do you add back depreciation for tax?

James Craig

Published Feb 21, 2026

Depreciation s counted as a cost that acts as a shield to diminish the tax effect. Then the depreciation charge is added back to after-tax earnings because it is a non-cash expense. Depreciation represents the declining economic value of an asset, but is not an actual cash outflow.

Why do you add back depreciation for tax?

A company’s depreciation expense reduces the amount of earnings on which taxes are based, thus reducing the amount of taxes owed. The larger the depreciation expense, the lower the taxable income, and the lower a company’s tax bill.

Why do you add back depreciation?

The use of depreciation can reduce taxes that can ultimately help to increase net income. The result is a higher amount of cash on the cash flow statement because depreciation is added back into the operating cash flow. Ultimately, depreciation does not negatively affect the operating cash flow of the business.

Do you have to claim depreciation on sale of business?

You don’t need to allocate gain on the sale of the property between the business or rental part of the property and the part used as a home. In addition, you don’t need to report the sale of the business or rental part on Form 4797. This is true whether or not you were entitled to claim any depreciation.

Where does depreciation recapture go on a 1040?

Depreciation recapture tax is reported on Schedule D of IRS Form 1040. With that in mind, it is not uncommon for property investors to avoid depreciation recapture tax entirely by investing the funds gained through the sale of one property immediately into a similar purpose.

When to claim depreciation on sale of rental property?

(This means you don’t have to work out ‘balancing adjustment event’ amounts for depreciating assets on sale of the rental property.) You can claim depreciation and capital works deduction for the tax year up to the date of rental property sale.

How does depreciation work on your tax return?

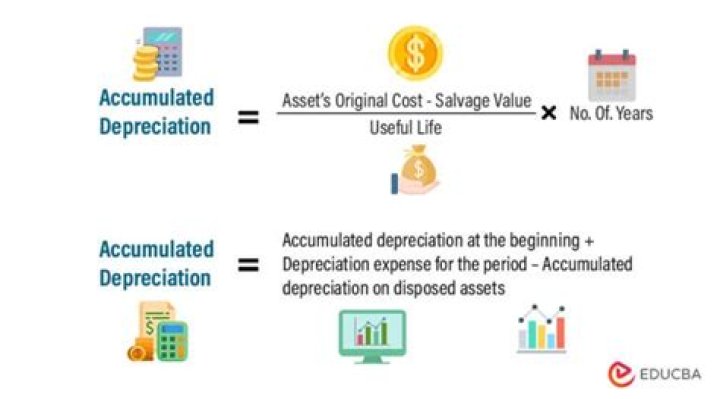

If you bought equipment for $30,000 and the IRS assigned you a 15% deduction rate with a deduction period of four years, your cost basis is $30,000. Your deduction expenses would be $4,500 per year. To determine the adjusted cost basis, you’d multiply four by your yearly deduction cost and subtract that from the cost basis.