Do mortgage lenders check tax records?

Henry Morales

Published Apr 12, 2026

Mortgage lenders will send relevant details of mortgage applications where they have inadequate evidence of declared income and suspect fraud using a secure electronic platform to HMRC, which will check income details declared to lenders against information provided in income tax and employment returns.

How do mortgage lenders check income?

Mortgage lenders verify employment by contacting employers directly and requesting income information and related documentation. Most lenders only require verbal confirmation, but some will seek email or fax verification. Lenders can verify self-employment income by obtaining tax return transcripts from the IRS.

Your tax documents give lenders information about your various types and sources of income and tell them how much is eligible toward your mortgage application. Any income that you report on your mortgage application that isn’t reported in your tax returns usually can’t be used to qualify.

Do mortgage lenders look at total income or taxable income?

Banks and lenders use gross income, not taxable income, to decide whether you qualify for a mortgage or other loan. Gross income is your before-tax earnings.

Is it normal for mortgage lenders to ask for more information?

The bottom line is there’s nothing unusual about being asked to provide more documents after you submit your application. It’s absolutely normal. The key is to be prepared to provide them as quickly as possible, so your loan can close on time. All of this seems very stressful, but it doesn’t need to be.

What information is a mortgage loan originator not allowed to ask a borrower who is applying for a home mortgage?

Lenders are not permitted to ask any questions that would discourage an applicant. Further, government regulations prevent mortgage lenders from denying loans based on race, color, religion, national origin, sex, marital status, age, or because you receive public assistance.

How do I show proof of mortgage payments?

Lenders’ requirements for proof of income for mortgage applications will differ. Typically, earned income is evidenced in the following ways: Payslips: The standard requirements are three months’ payslips and two years’ P60s although there are lenders who will accept less than this.

Do mortgage lenders check your employer?

Mortgage lenders usually verify your employment by contacting your employer directly and by reviewing recent income documentation. The borrower must sign a form authorizing an employer to release employment and income information to a prospective lender.

Are mortgage loans based on income?

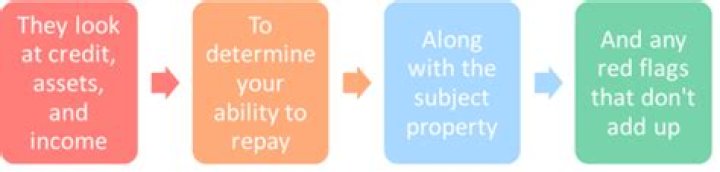

Many mortgage lenders rely on a debt-to-income (DTI) calculation to assess your ability to pay for a loan. This calculation compares your monthly gross income, typically from the income sources above, to your monthly debt load.

When do mortgage lenders ask for your tax return?

Most lenders will require self-employed borrowers to document their income through their tax returns. They will receive income as well as business-related expenses on the tax return. It is common for mortgage lenders to average this type of income for the previous two to three years.

What kind of tax forms do mortgage companies ask for?

Your mortgage lender will typically request a copy of your W2 tax forms, which will show your salary and compensation from your employer. However, the W2 form will not show all sources of income that you may receive.

Can you get a mortgage if you dont report income on your tax return?

Any income that you report on your mortgage application that isn’t reported in your tax returns usually can’t be used to qualify. Keep in mind that certain tax deductions may also decrease your income for loan purposes.

What kind of income do mortgage lenders ask for?

For example, rental property income, dividend income and even alimony or child support are just some of the many types of income that you can document through your tax returns. Most lenders will require self-employed borrowers to document their income through their tax returns.