Do I need a K1 to file my taxes?

Andrew Ramirez

Published Mar 25, 2026

To file your taxes, you must submit Form 1065 and Schedule K-1. The tax form reports the participation of each member in the business income, deductions, and tax credit items. But one-member LLCs must report as if they were a sole proprietorship, using Schedule C. In this case, they do not have to present Schedule K-1.

Are K-1 distributions taxable? Yes. If you’ve ever invested in a business such as partnership, C corporation, or LLC, or if you’re the beneficiary of a trust or an estate, then you’ve probably received a Schedule K-1 in the mail. Just like any other income, you need to report it, since it’s taxable income.

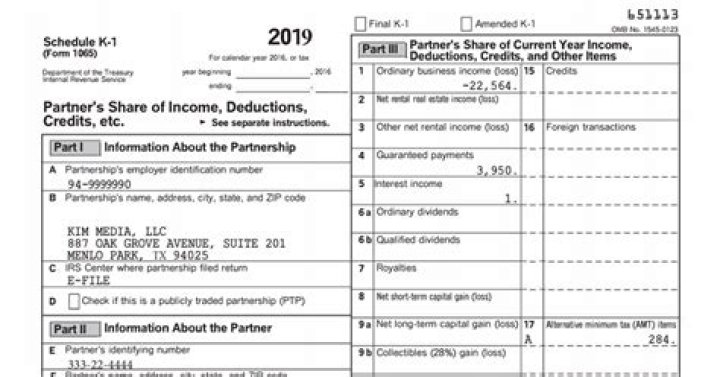

What do you need to know about Schedule K-1?

Schedule K-1 is the tax form used by partners and shareholders to report to the Internal Revenue Service their income, losses, dividends, or capital gains during the fiscal year. With this tax form, the business can also track the participation of each partner in the business’ performance, depending on how much capital was invested.

Where to report depreciation Adjustment on Schedule K-1?

For example, if the partnership reports a section 743(b) adjustment to depreciation for property used in its trade or business, report the adjustment on line 28 of Schedule E (Form 1040) in accordance with the instructions for box 1 of Schedule K-1.

How to prepare a schedule of loan amortization in Excel?

Let us take home loan example for preparing a schedule of Loan Amortization in Excel. Let us assume that a home loan is issued at the beginning of month 1. The principal is $1,500,000 the interest rate is 1% per month and the term is 60 months. Repayments are to be made at the end of each month.

How to report ” gain from loan repayments ” amount?

Ok. Assuming that this individual is maintaining your basis and understands how to arrive at the amount that is being reported on line 17 of your K-1, this is capital gain and reported on your 1040 Schedule D and applicable 8949. Just show the “gain” amount from line 17 as the proceeds with a zero cost basis.