Do I have to withdraw from my Roth IRA?

Henry Morales

Published Apr 01, 2026

You don’t. While traditional IRAs require that you take minimum withdrawals starting at age 70 ½, Roths have no mandatory withdrawal requirements. So if you retire and you have other assets to live off of, you can leave the money in your Roth and allow it to continue to grow for as long as you like.

Do Roth accounts also have a required minimum distribution?

Knowing what tax bracket you’ll be in when you start required minimum distributions is key. Unlike traditional IRAs and retirement plans, your Roth IRA isn’t subject to required minimum distributions starting at age 70 1/2.

Do you pay taxes on Roth IRA withdrawals?

With Roth IRAs, you pay taxes upfront, and qualified withdrawals are tax-free for both contributions and earnings.

Can you withdraw money from a Roth IRA at any time?

Contributions are the money you deposit into an IRA, while earnings are your profits. Both grow tax-free in your account. You can withdraw your Roth IRA contributions at any time, for any reason, with no tax or penalties. That’s because you make contributions with after-tax dollars, so you’ve already paid income taxes on that money.

Is there penalty for early withdrawal from Roth IRA?

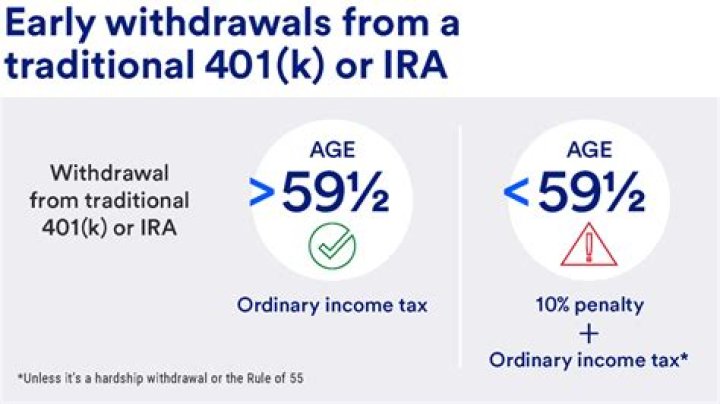

The withdrawal rules for Roth individual retirement accounts (IRAs) are generally more flexible than those for traditional IRAs and 401 (k)s. Still, you’ll want to do your homework before making any Roth IRA withdrawals. If you don’t meet certain requirements, you could end up owing taxes and a 10% early withdrawal penalty.

When do I have to start taking withdrawals from my IRA?

Withdrawals at age 70½ and beyond. Starting at age 70½, owners of Traditional IRAs must begin making withdrawals, also known as required minimum distributions (RMDs), from their accounts. These withdrawals are mandatory and violations incur severe penalties.

What’s the maximum amount you can withdraw from a Roth IRA?

Withdrawals from a Roth IRA you’ve had more than five years. You use the withdrawal (up to a $10,000 lifetime maximum) to pay for a first-time home purchase. You use the withdrawal to pay for qualified education expenses. You use the withdrawal for qualified expenses related to a birth or adoption.