Can you write off capital losses from previous years?

Sarah Duran

Published Apr 09, 2026

Realized capital losses from stocks can be used to reduce your tax bill. If you don’t have capital gains to offset the capital loss, you can use a capital loss as an offset to ordinary income, up to $3,000 per year. To deduct your stock market losses, you have to fill out Form 8949 and Schedule D for your tax return.

Do net capital losses expire?

Each year, the accumulated value of your capital losses becomes your net capital losses, which you may carry forward indefinitely. If you have not claimed your net capital losses by the time of your death, your representative can apply them to your final return to offset your capital gains for that year.

How to deduct capital losses from capital gains?

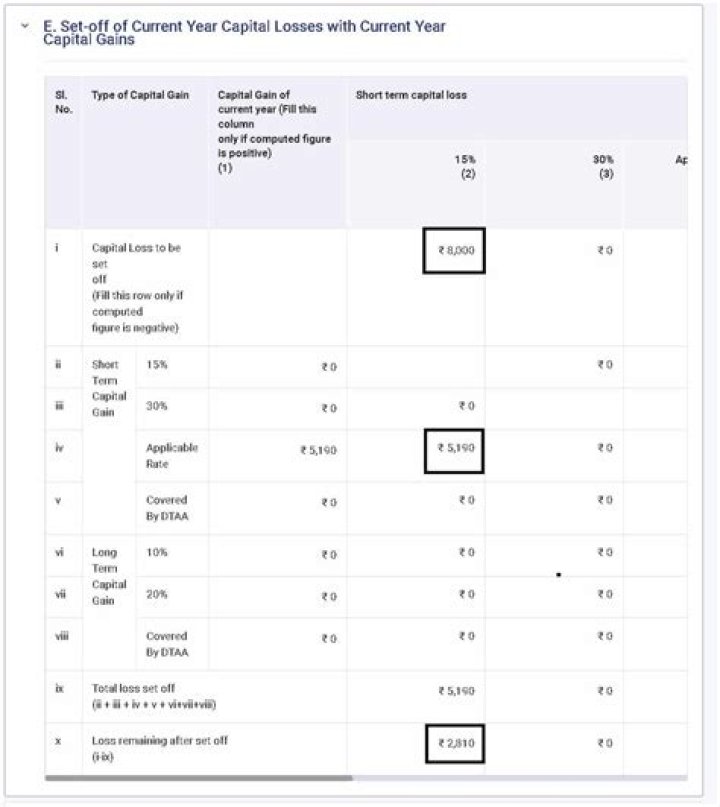

How to deduct capital losses Begin by deducting net capital losses from capital gains in the following order: First, reduce any gains subject to the 28% rate (e.g., gains on collectibles and qualified small business stock). Next, use any remaining loss to reduce gains subject to the 25% rate (e.g., unrecaptured Section 1250 gains).

What’s the maximum capital loss you can claim on taxes?

(1) The deduction limit for a net capital loss in any one year is $3,000. (2) If a capital loss exceeds $3,000 in any tax year the excess over $3,000 must be carried over to the next tax year.

When to use loss to reduce your gain?

Using losses to reduce your gain When you report a loss, the amount is deducted from the gains you made in the same tax year. If your total taxable gain is still above the tax-free allowance, you can deduct unused losses from previous tax years.

What are the rules for a capital loss?

9 Rules for Capital Losses (1) The deduction limit for a net capital loss in any one year is $3,000. (2) If a capital loss exceeds $3,000 in any tax year the excess over $3,000 must be carried over to the next tax year. (3) Treat the loss as if it was incurred in the carryover year.