Can you withdraw excess SEP contribution?

John Thompson

Published Feb 10, 2026

If you are covered by an SEP and your employer contributes too much to your account, you must withdraw the unwanted amount to avoid taxation and penalties. You should return the excess amount to your employer, but it’s not required.

What if I Overcontribute to my SEP?

You will have to file a Form 5330 and pay a 10% excise tax for each year until that $1,000 excess carryover was/is applied to available employer contribution space. The IRS will bill you for any penalties.

Can you withdraw excess contributions?

If you’ve contributed too much to your IRA for a given year, you’ll need to contact your bank or investment company to request the withdrawal of the excess IRA contributions. Depending on when you discover the excess, you may be able to remove the excess IRA contributions and avoid penalty taxes.

How do I withdraw excess IRA contributions?

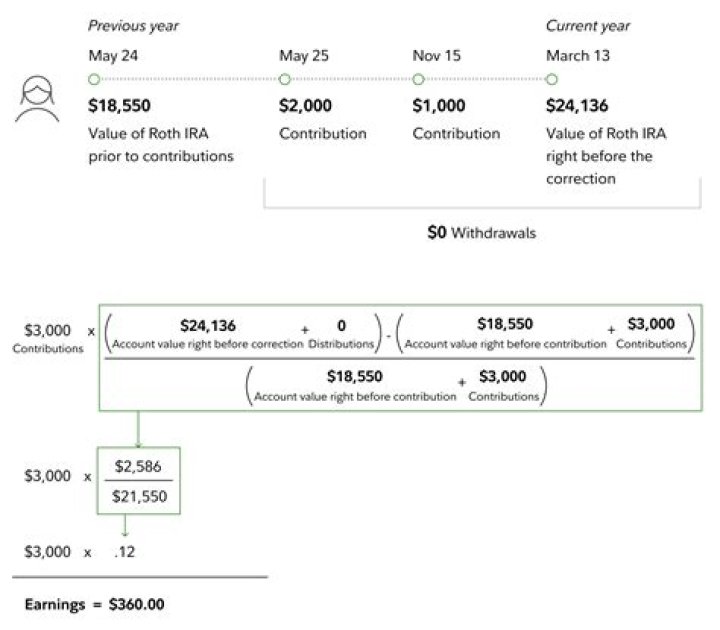

You can withdraw an excess contribution online by completing the appropriate DocuSign form. You can either: Remove the excess within 6 months and file an amended return by October 15—if eligible, you can also remove the excess plus your earnings by this date. Remove the excess once discovered, even after October 15.

What happens if you make a mistake on a SEP contribution?

If the mistake includes excess amounts contributed to the employees’ IRAs associated with the SEP, the employer must use VCP if the employer wishes to allow the excess amounts to remain in the affected participants’ IRAs. If this correction method is used, a special additional payment of at least 10% of the excess amount will apply.

Can a self employed person withdraw excess SEP contributions?

Client made an excess SEP contribution for 2018. He is self employed. Can he withdraw the excess amount without tax or penalty consequences? Solved! Go to Solution. 01-22-2020 05:37 PM The 2018 excess contributions need to be removed immediately, and they are subject to the penalty.

When to use VCP on a SEP contribution?

If the value of all IRAs exceeds $500,000, the user fee will be higher. If the mistake includes excess amounts contributed to the employees’ IRAs associated with the SEP, the employer must use VCP if the employer wishes to allow the excess amounts to remain in the affected participants’ IRAs.

What to do about excess SEP IRA contributions?

If any of the 2019 contributions were actually FOR 2018 (such as the Jan one for examply..) you might be able to manipulate one month’s contribution into *not* being in excess. Would be a bit of work, for likely not much gain, depending on the amounts.