Can you use cash basis for tax?

Emma Jordan

Published Feb 19, 2026

The most commonly used accounting methods are the cash method and the accrual method. Under the cash method, you generally report income in the tax year you receive it, and deduct expenses in the tax year in which you pay the expenses.

Can cash basis taxpayer deduct accrued expenses?

Expenses are deductible when the amount is actually paid. Under the Accrual method, income is recognized once the “all events test” has been met. For example, a cash-basis taxpayer can deduct an amount accrued for a profit sharing contribution, provided it is paid by the due date of the return.

Why is cash basis better for tax purposes?

Tax-planning flexibility. It offers greater flexibility to control the timing of income and deductions. Because income is taxed in the year it’s received, the cash method does a better job of ensuring that a business has the funds it needs to pay its tax bill.

Is accrual or cash basis better?

Cash basis accounting is easier, but accrual accounting portrays a more accurate portrait of a company’s health by including accounts payable and accounts receivable. The accrual method is the most commonly used method, especially by publicly-traded companies as it smooths out earnings over time.

Can a tax shelter use cash method of accounting?

If a taxpayer is found to be a tax shelter, it is not allowed to compute taxable income under the cash receipts and disbursements method of accounting. As one might expect, the term includes a partnership or other entity if a significant purpose is the avoidance or evasion of federal income tax.

Can I deduct inventory on cash basis?

Use of the cash basis does not mean that these businesses may write off inventory items when they pay for them. Instead, they may use a method of accounting for inventories that either treats them as non-incidental materials and supplies or follows the way their financial statements treat inventory.

Is tax shelter Legal?

Tax shelters are legal, and can range from investments or investment accounts that provide favorable tax treatment, to activities or transactions that lower taxable income through deductions or credits. Common examples of tax shelter are employer-sponsored 401(k) retirement plans and municipal bonds.

Is inventory a tax deduction?

Inventory isn’t a tax deduction. Inventory is a reduction of your gross receipts. This means that inventory will decrease your “income before calculating income taxes” or “taxable income.”

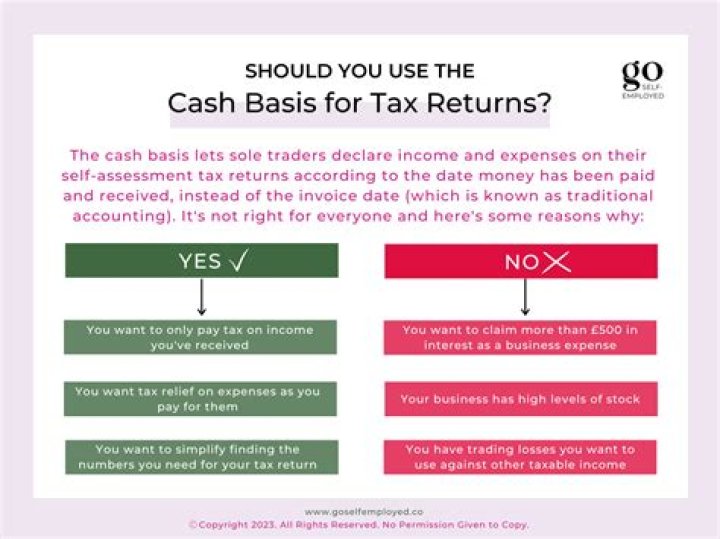

Should I tick cash basis for my tax return?

That’s it. Never tick the “Have you used a cash basis?” on the self-assessment tax return if you are doing the accruals basis, or if you’re doing it, you tend to know when you’ve raised the invoice, that’s when you’re accounting for it. Don’t tick the cash basis, because it may cause problems later on down the line.

Can A S corporation file on a cash basis?

Eligible S corporations can file on a cash basis if they have less than $10 million in annual gross receipts. S corporations that hold inventory can only use a cash basis if they have average annual gross receipts of less than $1 million. S corporations can maintain their accounting records on a cash basis or an accrual basis.

Can a corporation use the cash basis method?

Although taxpayers can choose any tax reporting method at their discretion, there are some entities prohibited from using the cash basis method. These taxpayers include: A corporation (other than an S corporation) with average annual gross receipts exceeding $5 million.

Can a tax return be on a cash basis?

If the tax return is on the cash basis and the books are on accrual basis you’ll spot the accounts receivable and/or accounts payable. And if you know how, you can then convert the income statement (front page of the tax return) from cash to accrual. So to answer the question, no…cash-basis on a tax return is not a red flag.

Can a farm corporation use the cash method?

For tax years beginning in 2019, farm corporations or partnerships that have average annual gross receipts of $26 million or less for the 3 preceding tax years and are not tax shelters can use the cash method instead of the accrual method. See publication 225, Farmer’s Tax Guide, for more information.