Can you roll a qualified plan into a Roth?

Mia Ramsey

Published Mar 09, 2026

More In Retirement Plans You can roll over eligible rollover distributions from these plans to a Roth IRA or to a designated Roth account in the same plan (if the plan allows rollovers to designated Roth accounts).

Can a 457b be rolled into an IRA?

457(b) ROLLOVER GUIDELINES your 457(b) plan to an IRA; you cannot make this rollover while you’re still working for the governmental unit or agency that provides you with the 457(b) plan. IRA, you will first need to check with your plan administrator to make certain this rollover option is permitted in your plan.

Is there a penalty for rolling over a 401k to a Roth IRA?

The ideal candidate for rolling an employer retirement fund into a new Roth IRA is a person who does not expect to take a distribution from the account for at least five years. There is a 10% penalty on money withdrawn from the Roth within five years of the date of the conversion.

Can a pension plan be rolled over to a Roth IRA?

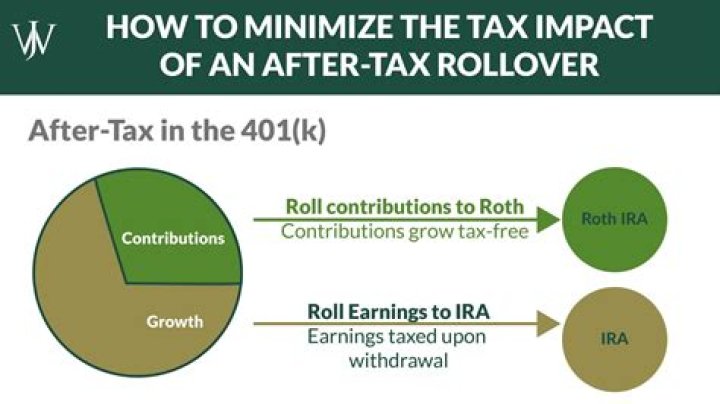

You generally can roll a pension lump sum into a Roth IRA, but that may not be a good idea. Another option is to roll the pension money directly into a traditional IRA, which creates no new tax bill, then gradually convert some of the money to a Roth every year.

What happens to my 457 B when I retire?

Once you retire or if you leave your job before retirement, you can withdraw part or all of the funds in your 457(b) plan. All money you take out of the account is taxable as ordinary income in the year it is removed. This increase in taxable income may result in some of your Social Security taxes becoming taxable.

What is the 5 year rule for Roth conversions?

The 5-year rule on Roth conversions requires you to wait five years before withdrawing any converted balances — contributions or earnings — regardless of your age. If you take money out before the five years is up, you’ll have to pay a 10% penalty when you file your tax return.

What happens to my deferred compensation if I quit?

Depending on the terms of your plan, you may end up forfeiting all or part of your deferred compensation if you leave the company early. That’s why these plans are also used as “golden handcuffs” to keep important employees at the company. They can’t be transferred or rolled over into an IRA or new employer plan.

Is deferred compensation considered earned income for Social Security?

For Social Security purposes, though, deferred compensation is counted when it’s earned — not when it’s received. So any money you receive from a deferred compensation plan while you’re between age 62 and your full retirement age doesn’t count against Social Security retirement benefits.

At what age can you withdraw from a 457 without penalty?

59 and a half years old

Money saved in a 457 plan is designed for retirement, but unlike 401(k) and 403(b) plans, you can take a withdrawal from the 457 without penalty before you are 59 and a half years old.

Does deferred compensation affect Social Security benefits?

Deferred compensation shouldn’t affect Social Security benefits. Generally, the Social Security Administration isn’t worried about payments that aren’t for work in the current period.