Can you pay interest upfront?

Mia Ramsey

Published Feb 19, 2026

You can pay for a lower interest rate on your mortgage upfront, but whether you should depends on the math. One option for homebuyers taking out a mortgage is to pay for a lower interest rate upfront. Buying down your rate means paying for mortgage points at the start of the loan to lower your rate.

Do you pay interest upfront on mortgage?

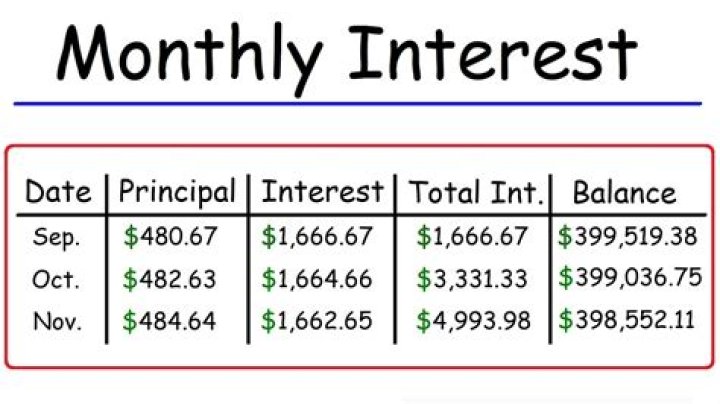

The amount you borrow with your mortgage is known as the principal. Each month, part of your monthly payment will go toward paying off that principal, or mortgage balance, and part will go toward interest on the loan. The part of the payment that goes to interest doesn’t reduce your balance or build your equity.

What part is paid off first in an amortized loan?

interest expense

An amortized loan payment first pays off the interest expense for the period; any remaining amount is put towards reducing the principal amount. As the interest portion of the payments for an amortization loan decreases, the principal portion increases.

Can you pay off a fully amortized loan early?

One of the simplest ways to pay a mortgage off early is to use your amortization schedule as a guide and send you regular monthly payment, along with a check for the principal portion of the next month’s payment. Using this method cuts the term of a 30-year mortgage in half.

What kind of a loan would be fully paid out over the life of the loan?

Fully amortized loans

Fully amortized loans have schedules such that the amount of your payment that goes toward principal and interest changes over time so that your balance is fully paid off by the end of the loan term.

What happens when a loan is negatively amortized?

Negative amortization means that even when you pay, the amount you owe will still go up because you are not paying enough to cover the interest. The unpaid interest gets added to the amount you borrowed, and the amount you owe increases.

What kind of a loan would be fully paid out over the life of the loan quizlet?

package mortgage. What kind of a loan would be fully paid out over the life of the loan? A Budget Mortgage is a loan, which has a payment composed of the following? balloon or a partially amortized loan.

What can happen if you do not make your balloon payments for your loan?

The balloon payment is equal to unpaid principal and interest due when a balloon mortgage becomes due and payable. If the balloon payment isn’t paid when due, the mortgage lender notifies the borrower of the default and may start foreclosure.

How do you calculate upfront interest?

Add-on interest is a method of calculating the interest to be paid on a loan by combining the total principal amount borrowed and the total interest due into a single figure, then multiplying that figure by the number of years to repayment. The total is then divided by the number of monthly payments to be made.

Residential loans

Residential loans are amortized over the life of the loan so that the loan is fully repaid at the end of the loan term. Unlike residential loans, the terms of commercial loans typically range from five years (or less) to 20 years, and the amortization period is often longer than the term of the loan.

What happens to the interest on an amortizing loan?

The lender will then deduct the interest amount owed from the monthly periodic payment, and the remainder of the payment will go towards the payment of the principal. As the periodic payment reduce the loan balance, the portion of the loan that goes towards interest payment also decreases.

How is principal paid back on a non amortizing loan?

A non-amortizing loan does not come with an amortization schedule. Typically, a loan’s principal will get paid back in installments. For example, most house mortgages are paid in this way. However, the principal on non-amortizing loans is paid back in a lump sum.

How to avoid an upfront interest loan?

Hopefully after you have read it, you will avoid upfront interest loans, regardless of how “low” the interest rate being offered is, so that you do not become poorer the instant you sign up and the loan is approved.