Can you have a 457 B and a Roth IRA?

Andrew Mclaughlin

Published Apr 09, 2026

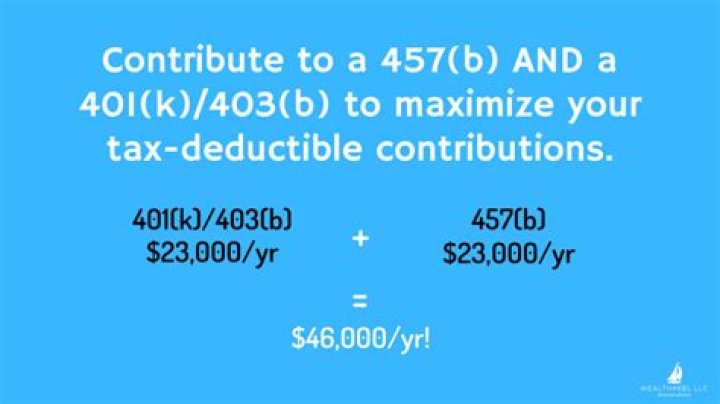

You Can Max out Both a 457 and a Roth IRA In fact, having both types of retirement accounts can serve as a hedge against the unpredictability of future tax rates. If tax rates are a lot higher when you retire, you will have significantly benefited from your Roth IRA because your withdrawals are tax-free.

How does a Roth 457b work?

When you choose to make Roth 457(b) contributions, you’ll pay taxes upfront when your money goes into the plan. Then you’ll enjoy tax-free withdrawals — as long as you’re at least 59½, and do not take withdrawals from your Roth account for at least five years after your first Roth contribution is made to the plan.

Should I roll over my 457b?

Your funds in such a plan can only be rolled over into another non-governmental 457 plan. With a 457(f) plan, the limits are similar: You may not roll over funds from a 457(f) plan to any other type of tax-deferred fund.

Can I take money out of my 457b?

Money saved in a 457 plan is designed for retirement, but unlike 401(k) and 403(b) plans, you can take a withdrawal from the 457 without penalty before you are 59 and a half years old. There is no penalty for an early withdrawal, but be prepared to pay income tax on any money you withdraw from a 457 plan (at any age).

How can I take money out of my 457?

Unlike other retirement plans, under the IRC, 457 participants can withdraw funds before the age of 59½ as long as you either leave your employer or have a qualifying hardship. You can take money out of your 457 plan without penalty at any age, although you will have to pay income taxes on any money you withdraw.

Can you contribute to a Roth 457 ( b ) plan?

A Roth 457(b) plan is a voluntary retirement plan. Technically, it is a supplemental tax-deferred retirement savings plan. The Internal Revenue Service allows employees of school districts, local governments, and tax-exempt organizations to take part in a Roth 457(b) plan. With a Roth 457(b), you contribute on an after-tax basis.

How old do you have to be to withdraw from Roth 457 plan?

However, in order for a withdrawal from a Roth 457 contribution to be tax-free, the plan participant must be older than 59 1/2. In addition, the first contribution to the Roth 457 plan has to have been made at least five years before the withdrawal. It is easier to understand with a quick table: All withdrawals from a regular 457 plan are taxable.

Do you need to know the details of your 457 ( b )?

You need to know all the details of your 457 (b) prior to deciding to use it or not. Most importantly is your plan governmental or not. (Why two plans with very different rules have the same name is beyond me.) If your offering is a governmental 457 (b) I’d count my lucky stars and treat it as an extra 403 (b).

How does a 457b deferred compensation plan work?

The organization must be a state or local government or a tax-exempt organization under IRC 501 (c). How do 457 (b) plans work? Employers or employees through salary reductions contribute up to the IRC 402 (g) limit ($19,500 in 2021 and in 2020; $19,000 in 2019) on behalf of participants under the plan.