Can you gift appreciated stock to a family member?

Henry Morales

Published Mar 24, 2026

Gifts of stock can be made in lieu of giving cash. The annual gifting limits of $15,000 per person ($30,000 for a joint gift with your spouse) apply, and the value of the stock on the day of the transfer constitutes the amount of the gift.

Stocks can be given to a recipient as a gift whereby the recipient benefits from any gains in the stock’s price. Giving the gift of a stock can also provide benefits for the giver, particularly if the stock has appreciated in value since the giver can avoid paying taxes on those earnings or gains.

Do I have to pay taxes on a gift of stock?

The recipient of a gift does not pay tax on any gift valued at $11,000 or less, no matter if it is a boat, car, cash, or stock. This means you don’t owe taxes at the time of the gift of the stock. When the recipient sells the stock, however, it is a taxable event.

Can I transfer stock to my parents?

Yes, you can gift stock directly You can transfer it directly from one brokerage account to another. You don’t mention your daughter’s age, but even if she were a minor, you could open a custodial account for her and make the stock transfer.

How do I gift stock to a family member?

You can start the process online in your own brokerage account by opting to gift shares or securities you own; if you can’t find that option, contact your brokerage firm directly. If you want to gift a stock you don’t already own, you’ll have to purchase it in your account, then transfer it to the recipient.

How do you transfer stock to a family member after death?

To facilitate a transfer, the executor will need a copy of the decedent’s will or a letter from the probate court confirming that the beneficiary in question is indeed the person entitled to receive the shares. The executor must then send these documents to a transfer agent, who can complete the transfer of ownership.

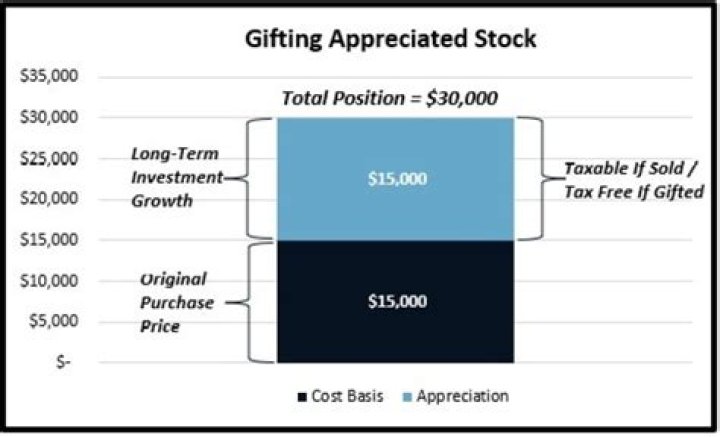

What happens if I gift appreciated stock?

By gifting appreciated stock, you avoid any long-term capital gains tax liability that you would otherwise owe in the future. Any capital gain liability does transfer to the recipient of your gift – there is no “step-up” in cost basis when gifting stock; this occurs only at death.

Is it better to gift cash or stock?

The Better Idea: Gift cash or stock that has minimal appreciation. Therefore, you should hold onto highly appreciated stock and bequeath it after your passing so its cost basis “steps up” upon your death.

What is the cost basis of a gifted stock?

The cost basis of stock you received as a gift (“gifted stock”) is determined by the giver’s original cost basis and the fair market value (FMV) of the stock at the time you received the gift. If the FMV when you received the gift was more the original cost basis, use the original cost basis when you sell.

What should I consider when gifting stock to a family member?

When gifting stock to a child or family member, make sure you’re considering the cost basis rather than the current value. The cost basis of cash is the value of the cash when gifted. To illustrate: If the person making the gift (the donor) gifts $15,000 cash to the person receiving the gift (the donee), the cost basis of the gift would be $15,000.

Can you gift appreciated stock to a child in California?

High income parents subject to California’s 37.1% capital gains tax rate could gift shares of appreciated stock to their children living in Washington who could then sell the stock and not be subject to any capital gains tax.

How old do you have to be to gift appreciated stock?

But in 2006 Congress raised the kiddie tax such that dependents up to age 23 are subject to their parent’s tax rate on investment assets if they are full time students. However, for children age 24 and over gifting appreciated stock may result in some significant generational financial planning to reduce the extended family’s taxes owed.

How many children can you gift stock to?

In addition, Senior has a wife who will join in this gift, which will allow for a second $13,000 exclusion. So the taxable gift to each child is reduced by another $26,000. Additional savings to the family are $23,400 (45% x $26,000 x 2 children).