Can you do a like-kind exchange on a personal residence?

Sarah Duran

Published Mar 28, 2026

Normally the IRS does not allow you to conduct a 1031 exchange with your primary residence. That’s because the home that you live in isn’t being used as an investment property or being held for business purposes. Instead, your primary residence is used to provide shelter for your family.

Can you do a like-kind exchange on land?

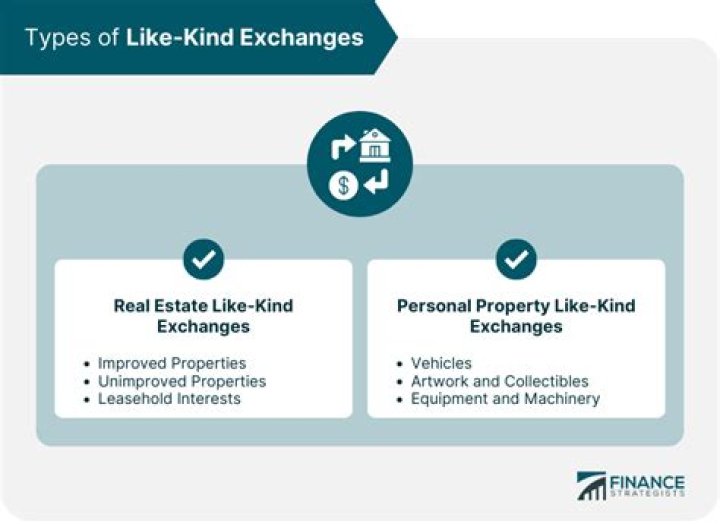

Most exchanges must merely be of “like-kind”—an enigmatic phrase that doesn’t mean what you think it means. You can exchange an apartment building for raw land, or a ranch for a strip mall. The rules are surprisingly liberal. You can even exchange one business for another.

Can I do a 1031 exchange on personal property?

Personal Property as a 1031 Exchange While most 1031 exchanges involve real property, personal property may be exchanged as well. Personal property does not mean property used for personal gain because IRC 1031 requires all property, whether real or personal, to be used for business, trade or investment.

Who is eligible for 1031 like kind property exchange?

Any tax payer who uses a property in their business or as an investment can take advantage of the 1031 exchange. In a typical IRS qualified §1031 like-kind property exchange, investors defer paying capital gains, depreciation recapture, and income taxes on commercial investment property when it’s sold.

When does like kind exchange become real property?

In response to this change, questions arose on what was defined as “real property” and whether a like-kind exchange would fail if incidental personal property was received. On June 11, 2020, these questions were answered by Treasury through its release of proposed regulations (REG-117589-18).

Can a like kind exchange be a taxable event?

Because of this change, the exchange of personal property for other personal property of like kind is now a taxable event. In response to this change, questions arose on what was defined as “real property” and whether a like-kind exchange would fail if incidental personal property was received.

Can a personal property be treated as like-kind property?

If the purchase price is allocated to personal property and the amount is less than 15% of FMV of the real property, the proposed regulations indicate that even though the exchange will not fail to be treated as of like-kind property, there will be gain recognition for the FMV of the personal property.