Can you capitalize interest under GAAP?

James Craig

Published Feb 19, 2026

Under US GAAP, interest income on any temporary investment of funds pending expenditure on the asset is not generally offset against interest costs in determining either the capitalization rates or limitations on the amount of interest to be capitalized.

What can be capitalized under GAAP?

GAAP allows companies to capitalize costs if they’re increasing the value or extending the useful life of the asset. For example, a company can capitalize the cost of a new transmission that will add five years to a company delivery truck, but it can’t capitalize the cost of a routine oil change.

How is capitalized interest accounted for?

Capitalized interest is an accounting practice required under the accrual basis of accounting. Instead, capitalized interest is treated as part of the fixed asset or loan balance and is included in the depreciation of the long-term asset or loan repayment.

Can interest expense be capitalized?

Unlike an interest expense incurred for any other purpose, capitalized interest is not expensed immediately on the income statement of a company’s financial statements. Instead, firms capitalize it, meaning the interest paid increases the cost basis of the related long-term asset on the balance sheet.

What is the purpose of capitalization?

Capitalization Like punctuation, capitalization helps convey information. The first word of every sentence is capitalized, signaling that a new sentence has begun. Proper nouns – the name of a particular person, place, or thing – are capitalized to indicate uniqueness.

What is the difference between accrued interest and capitalized interest?

What Is Capitalized Interest? It is usually compound interest for a loan taken to acquire or construct long-term assets. The amount of capitalized interest is the amount of accrued interest on the compound interest owed; an accrued amount is the portion of interest that hasn’t been paid since the last payment.

Why does GAAP allow a calculation for interest capitalization?

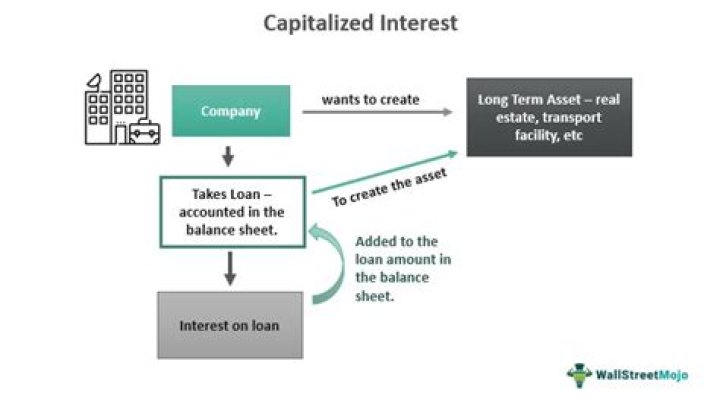

Understanding Capitalized Interest Because many companies finance the construction of long-term assets with debt, Generally Accepted Accounting Principles (GAAP) allow firms to avoid expensing interest on such debt and include it on their balance sheets as part of the historical cost of long-term assets.

How do you account for capitalized interest?

When a company capitalizes accrued interest, it takes the total amount of interest it owes on a long-term asset or loan balance since the last payment, and capitalizes it by adding the total interest owed to the total cost of the long-term asset or loan balance.

What is capitalized interest GAAP?

Capitalized interest is the cost of the funds used to finance the construction of a long-term asset that an entity constructs for itself. The capitalization of interest is required under the accrual basis of accounting, and results in an increase in the total amount of fixed assets appearing on the balance sheet.

Is it permissible to capitalize interest cost of assets?

However, interest cannot be capitalized for inventories that are routinely manufactured or otherwise produced in large quantities on a repetitive basis. The amount capitalized is to be an allocation of the interest cost incurred during the period required to complete the asset.

How is capitalized interest treated in a cash flow statement?

The interest is capitalized in order to accurately measure the cost of the asset. In the cash flow statement, the capitalized interest is shown as outflow under investing activities. Since capitalizing interest, reduces the interest expense, it increases the interest coverage ratio (EBIT/interest expense).

What does it mean for interest to capitalize?

Interest capitalization occurs when unpaid interest is added to the principal amount of your student loan. When the interest on your federal student loan is not paid as it accrues (during periods when you are responsible for paying the interest), your lender may capitalize the unpaid interest.

What does capitalize interest mean?

Interest capitalization occurs when unpaid interest is added to the principal amount of your student loan. Interest is then charged on that higher principal balance, increasing the overall cost of the loan (since interest will now be charged on the higher principal amount).

How are assets capitalized in accordance with GAAP?

Assets that are constructed or produced 1. Amount to be capitalized 2. Total amount of interest cost capitalized 1. Specific borrowings for the construction 2. For the average accumulated expenditures over the specific borrowings 1. Capitalization begins when (1), (2), (3) occur 2. Capitalization ends when (4) and (5) occur

When to capitalize interest cost in an acquisition?

When to capitalize interest cost. Interest is capitalized in order to obtain a more complete picture of the total acquisition cost associated with an asset, since an entity may incur a significant interest expense during the acquisition and start-up phases of the asset.

How are borrowing costs capitalized under IAS 23?

IAS 23 requires the capitalization of interest and certain other costs that are directly attributable to the acquisition or construction of ‘qualifying assets’. Companies apply the following step-by-step analysis to determine the borrowing costs to be capitalized.

Which is an example of capitalized interest accounting?

For example: At 5 percent interest rate the $100,000 loan which is borrowed to construct windmills. It takes one year to complete the construction. This implies that the cost of the windmill will not only include the initial cost of asset but also the interest expense required to be paid off for the load.