Can partnerships deduct capital losses?

John Thompson

Published Mar 27, 2026

A partnership, therefore, must apply the deductible loss limitation of section 165(c) when computing its tax items for any given year, and is thus only entitled to deductions for trade or business losses, investment losses, and casualty losses.

Can partnership losses offset ordinary income?

Losses Passed Through to Partners Losses are passed through to the partners. These losses may take the form of a business ordinary income loss for the year or a capital loss on the sale of property during the year.

Can you deduct an ordinary loss?

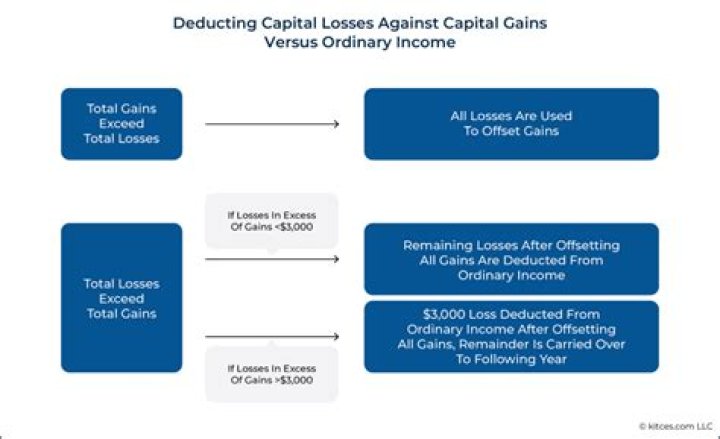

Ordinary Losses for Taxpayers An ordinary loss is mostly fully deductible in the year of the loss, whereas capital loss is not. An ordinary loss will offset ordinary income and capital gains on a one-to-one basis. A capital loss is strictly limited to offsetting a capital gain and up to $3,000 of ordinary income.

Are partnership losses ordinary or capital?

Reg. §1.165-2 stating that, absent a sale or exchange, a loss resulting from the abandonment or worthlessness of non-depreciable property, such as a partnership interest, qualifies as an ordinary loss even in the case of capital assets.

Can LLC losses offset personal income?

If your business is operated as an LLC, S corporation, or partnership, your share of the business’s losses are passed through the business to your individual return and deducted from your other personal income in the same way as a sole proprietor.

Can you use business losses to offset ordinary income?

The difference in treatment between business losses and capital losses is that business losses may offset ordinary income with any excess creating an NOL, whereas capital losses may only be offset against capital gains plus up to $3,000 of ordinary income.

What is an ordinary loss vs capital loss?

A capital loss results when you sell a capital asset, such as stocks and bond, for less than your cost. An ordinary loss occurs from the normal operations of a business when expenses exceed income. When capital losses exceed capital gains a net capital occurs.

Can I carry back a capital loss?

For a corporation, capital losses are allowed in the current tax year only to the extent of capital gains. A net capital loss is carried back 3 years and forward up to 5 years as a short-term capital loss. Foreign expropriation capital losses cannot be carried back, but are carried forward up to 10 years.

Can a partner claim a loss as a capital loss?

Given this limitation on capital loss deductions, it is usually more beneficial to characterize the loss as ordinary rather than capital. While a partnership may not be prepared to abandon its assets, courts have permitted a partner to abandon his or her partnership interest or claim a loss from its worthlessness.

Can a partnership loss be deductible on a tax return?

In order to deduct these losses, partners may be tempted to guarantee partnership debt. Depending on the type of partnership, limited partnership (LP) or limited liability company (LLC), the impact on the at risk limitation can be different than the desired result.

When is the loss of a partnership an ordinary loss?

If no consideration is paid to the taxpayer, the loss is generally all ordinary loss because there is no sale or exchange of the partnership interest. If the taxpayer is relieved of liabilities, the debt relief constitutes consideration in exchange for the partnership interest, and the loss is a capital loss.

Can a partnership loss be deducted on a Schedule K-1?

When an individual receives a Schedule K-1 from a partnership reflecting a loss, there are several things to consider before deciding if the loss can be deducted. In order to determine deductibility, a partner’s basis and at risk limitations need to be evaluated. See original Article here from Accounting Today>