Can I sell my 1031 Exchange property?

Henry Morales

Published Mar 04, 2026

The most important thing to know is that personal property is excluded from 1031 exchanges. You can’t sell an investment property, buy a property you intend to live in, and avoid paying capital gains tax on your profits.

How long after a 1031 Exchange can you sell?

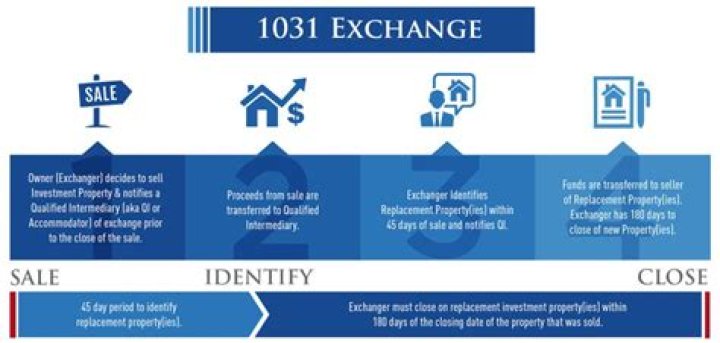

Specifically, you have 45 days from the date you relinquish your asset to find a “like-kind” replacement. And, you have 180 days from the date you relinquish Real Estate A to close on that replacement Real Estate B. These timelines are chiseled in IRS stone, with no exceptions.

Can I do a 1031 Exchange on property I already own?

YES, it is possible to improve property ALREADY OWNED by a 1031 Exchange! An improvement exchange just means we are going to buy something and build on it… Hear it all from the best 1031 Exchange facilitator in the business, David Moore.

Can you do a 1031 Exchange before you sell?

If you follow all of the IRS rules for a “Reverse 1031 Exchange,” then yes, it is possible to acquire property in a like-kind exchange before selling the property given up. These transactions allow you to reinvest all of your proceeds into the new property rather than paying the tax on the gain.

When is the right time to sell my 1031 exchange property?

How does a deferred exchange qualify under Section 1031?

They allow you to dispose of property and subsequently acquire one or more other like-kind replacement properties. To qualify as a Section 1031 exchange, a deferred exchange must be distinguished from the case of a taxpayer simply selling one property and using the proceeds to purchase another property (which is a taxable transaction).

Can a dwelling unit be included in a 1031 sale?

However, the term “dwelling unit” does not include other structures on the property. Revenue Procedure 2005-14 points out that neither Section 121 nor 1031 addresses the potential for applying both sections to one sale of a property.

What does section 1031 of the Internal Revenue Code mean?

Section 1031 of the Internal Revenue Code allows a taxpayer to defer the recognition of gains (or losses) on an investment property when sold if the relinquished property is exchanged for a like-kind replacement property.