Can both spouses do Roth conversion?

Ava Robinson

Published Apr 05, 2026

Provided they meet the specific federal requirements for being allowed to contribute to a Roth, each spouse in a marriage may contribute money toward a Roth IRA in his or her own name. Couples may not both contribute to a single IRA listed with both their names, but rather must maintain their own Roth IRA accounts.

Can I contribute to a Roth IRA if my spouse works?

There is no special type of IRA for spouses, instead the rule allows non-working spouses to contribute to a traditional IRA or a Roth IRA—provided they file a joint tax return with their working spouse. Individual retirement accounts opened under the spousal IRA rules are not co-owned.

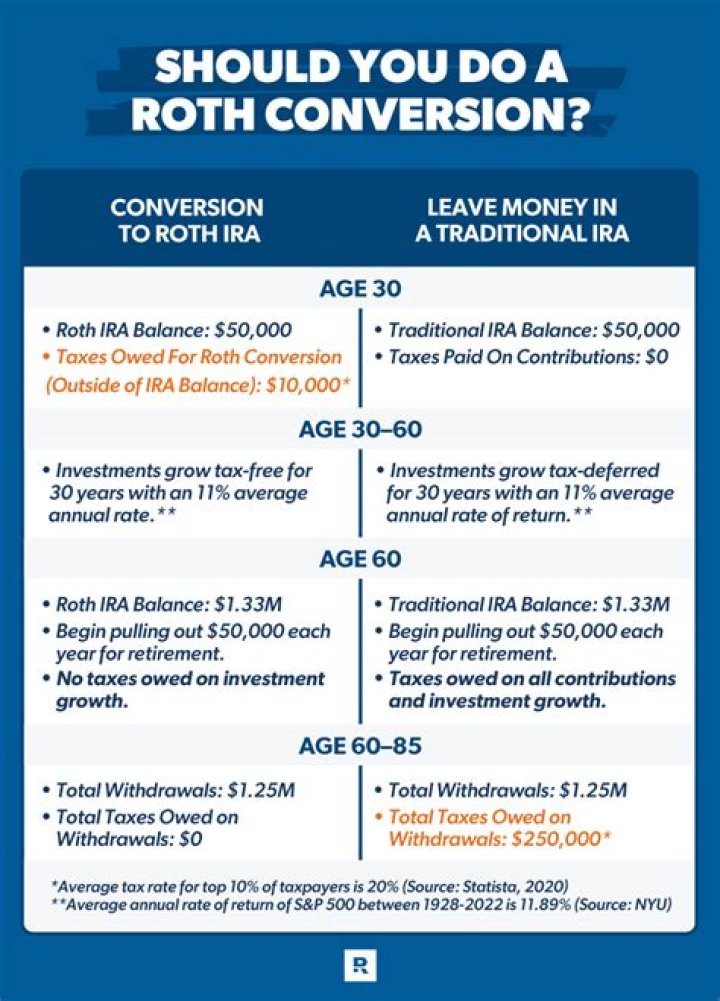

When is it time to consider a Roth conversion?

A series of lifetime Roth conversions can be especially attractive for married taxpayers where one spouse has a potentially fatal illness or condition and the other anticipates about the same pretax income after death but a higher tax liability from the effects of a higher single tax bracket and lower standard deduction or other factors.

Do you have to pay taxes on a Roth IRA conversion?

Even if your income exceeds the limits for making contributions to a Roth IRA, you can still do a Roth conversion, sometimes called a “backdoor Roth IRA.” You will owe taxes on the money you …

Who are the best people to convert to a Roth IRA?

Greg Daugherty has worked 25+ years as an editor and writer for major publications and websites. He is also the author of two books. David Kindness is an accounting, tax, and finance expert. He has helped individuals and companies worth tens of millions achieve greater financial success. Does a Roth IRA Conversion Make Sense for You?

What happens to gross income when you convert to Roth?

Because direct rollovers of eligible rollover distributions to multiple destinations at the same time are treated as a single distribution for purposes of allocating pretax and after – tax amounts, his gross income attributable to the distribution will be zero. Several considerations are unique to conversions from qualified retirement plans.