Can a 529 pay for off campus housing?

John Thompson

Published Mar 09, 2026

Can I Be Reimbursed By 529 For Off-Campus Living? The short answer is: Yes, room and board expenses for off-campus housing – including a parent’s home – may be reimbursed through a 529 plan, but not necessarily the full cost.

Can 529 plans be used for room and board?

While investors can use 529 funds to pay for a college’s room and board fees, housing arrangements off campus also count. Since room and board costs are qualified expenses, that means students with an on-campus meal plan can pay for it with 529 funds.

What expenses can I use 529 funds for?

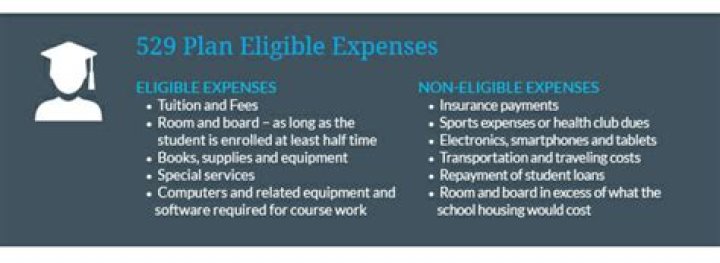

Money from a 529 account can be used for major post-secondary education costs such as: Required tuition, fees, books, supplies and equipment. Certain room and board expenses, which may include food purchased directly through the college or university (for the stipulations of off-campus living — see below)

Can a 529 be used for anything other than education?

A 529 account can be used for other types of education besides college, including trade and vocational schools and more. However, if you decide to use the money for something other than qualified education expenses, you will have to pay income taxes plus a 10% penalty on the earnings.

Do I need receipts for 529 expenses?

You don’t need to provide the 529 plan with evidence that you will be using the money for eligible expenses, but you do need to keep the receipts, canceled checks and other paperwork in your tax records (see When to Toss Tax Records for more information), in case the IRS later asks for evidence that the money was used …

What can 529 funds be used for 2021?

What expenses can you use a 529 Plan for?

- College Tuition and Fees.

- Vocational and Trade School Tuition and Fees.

- Elementary or Secondary School Tuition.

- Room and Board.

- Food and Meal Plans.

- Books and Supplies.

- Electronic Devices.

- Computer Software.

Which is better 529 or UTMA?

Any UTMA account assets are counted as the designated beneficiary’s, while the 529 plan assets are counted as the parent’s on the FAFSA form. It is harder for a child to qualify when the assets are theirs, so UTMA accounts are less advantageous than 529 plans when it comes to qualifying for financial aid .

What documentation is needed for 529 withdrawal?

Form 1099-Q

In each year you take withdrawals from a 529, the plan administrator should issue a Form 1099-Q, which reports the total distribution taken from the account in a given year, the portion of the distribution that came from earnings in the account, and the portion of the distribution that represents the original …

Does 1099-q get reported on parent’s return?

When the Form 1099-Q is issued to the 529 plan beneficiary, any taxable amount of the distribution will be reported on the beneficiary’s income tax return. This typically results in a lower tax obligation than if the Form 1099-Q is issued to the parent or 529 plan account owner.

Do I have to pay taxes on 529 distributions?

529 withdrawals are tax-free to the extent your child (or other account beneficiary) incurs qualified education expenses (QHEE) during the year. If you withdraw more than the QHEE, the excess is a non-qualified distribution. The principal portion of your 529 withdrawal is not subject to tax or penalty.

How much can a grandparent contribute to a 529 plan?

You can front-load a 529 plan (giving 5 years’ worth of annual gifts of up to $15,000 at once, for a total of up to $75,000 per person, per beneficiary) without having to pay a gift tax or chip away at the lifetime gift tax exclusion.

What happens to UTMA when child turns 21?

Virtually all states have adopted some form of UTMA that allows you to make gifts to a minor to be held in the name of a custodian during the age of minority. On reaching the age of majority, usually 21 years, the minor is entitled to all assets held in the account.

Who pays the taxes on a UTMA account?

Because money placed in an UGMA/UTMA account is owned by the child, earnings are generally taxed at the child’s—usually lower—tax rate, rather than the parent’s rate. For some families, this savings can be significant. Up to $1,050 in earnings tax-free. The next $1,050 is taxable at the child’s tax rate.

Do I have to pay taxes on 1099-Q?

For most qualified education program beneficiaries, the amounts reported on the 1099-Q aren’t reported on a tax return. Your adjusted expenses are $8,000—which means you don’t have to report any education program distributions on your tax return.

Do I need to include 529 distributions on my tax return?

When 529 plan funds are used to pay for qualified education expenses there is usually nothing to report on your federal income tax return.