Are royalties included in cost of goods sold?

Andrew Mclaughlin

Published May 18, 2026

The final regulations also clarify that sales-based royalties that a taxpayer allocates entirely to inventory property sold are included in cost of goods sold and may not be included in determining the cost of goods on hand at the end of the taxable year regardless of the taxpayer’s cost flow assumption.

What is Schedule 1125 A?

Purpose of Form. Use Form 1125-A to calculate and deduct cost of goods sold for certain entities. Who Must File. Filers of Form 1120, 1120-C, 1120-F, 1120S, or 1065, must complete and attach Form 1125-A if the applicable entity reports a deduction for cost of goods sold.

Can you capitalize cost of goods sold?

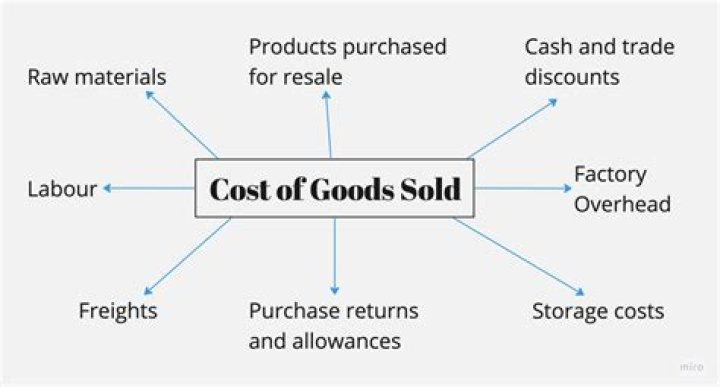

Overview. Many businesses sell goods that they have bought or produced. When the goods are bought or produced, the costs associated with such goods are capitalized as part of inventory (or stock) of goods. These costs are treated as an expense in the period the business recognizes income from sale of the goods.

Do you have to report inventory on Schedule C?

Although you are not required to report inventory if your receipts are 1 million or less as a Qualifying Taxpayer, the costs for what would otherwise be inventoriable items are considered to be NON-incidental materials and supplies to be listed on line 36 (purchases on Sch C). …

How are royalties classified as a selling expense?

Royalties are a share of the sale price and should be classified as a selling expense more than a cost of goods. The cost of your goods sold is not a factor of the royalty paid. The royalty is a factor of the selling price only.

Is there an exception to sales based royalty?

A royalty that serves as consideration for any other type of licensing arrangement does not qualify for the exception. Criterion 1: Sales- and Usage-Based Royalties. Generally, consideration in a sales-based royalty agreement is contingent upon and paid out as the licensee sells goods or services that utilize the licensed IP.

How are sales-based royalties and vendor allowances calculated?

The amount of the royalty was a percentage of the sales of the plastic products manufactured through the patented system. The taxpayer expensed these royalties currently. The court held, however, that Regs. Sec. 1.263A-1 (e) (3) (ii) (U) requires capitalization of the royalties as license and franchise costs.

How are sales based royalties capitalizable under Sec 263A?

Sales-based royalties are capitalizable indirect costs under Sec. 263A, as clarified by final regulations published in 2014 (T.D. 9652). Under the final regulations, if a taxpayer has sales-based royalties that must be capitalized under Sec. 263A, the taxpayer can choose to allocate sales-based royalties entirely to property that has been sold.