Are investment fees deductible on 1041?

James Craig

Published May 17, 2026

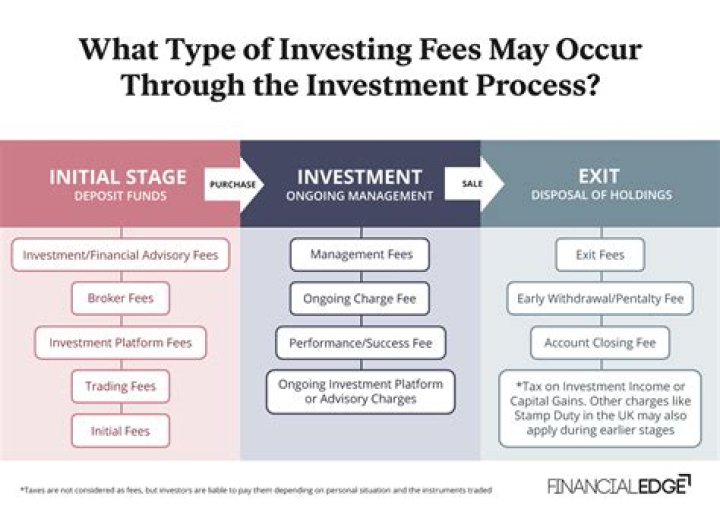

Are investment management fees deductible on form 1041, like on line 15a Other Deductions? No. The TCJA suspended the deduction for miscellaneous itemized deductions for individuals until 2025. Therefore, estates and trusts can no longer deduct investment advisor fees either.

Do I report investments on taxes?

You typically only have to pay taxes on the sale of investments when you receive a gain. To figure this out, you have to subtract the cost basis of your investment, which is normally what you paid, from the sale price to see if you had a gain. If you have a gain on the sale, you’ll have to see if you owe taxes.

Are investment fees deductible on a trust return?

The issue for these trusts is that the TCJA cut out miscellaneous itemized deductions for everyone, but trusts have no standard deduction to fall back on like individual taxpayers do. Pre-TCJA, for an individual, these fees were deductible to the extent they exceeded 2% of adjusted gross income.

What kind of income is reported on Form 1041?

IRS Form 1041 reports the income of trusts and estates. It’s similar to the Form 1040 tax return for individuals, and estates and trusts can take certain deductions.

When to use IRS Form 1041 for estate?

IRS Form 1041 is used to declare the income of an estate or trust but it’s not a substitute for filing personal income taxes on behalf of a deceased person. Loading Home Buying

Do you have to file a Schedule D on Form 1041?

Schedule D must also be submitted with the Form 1041. Keep in mind that these rules apply only to federal taxation. States have their procedures and laws, so check with a local accountant or tax attorney to find out if your estate or trust must pay income taxes at the state level as well.

When does a living trust have to file Form 1041?

The trustee of a living trust must file Form 1041 under section 641 of the Internal Revenue Code if it’s a domestic trust and if it has any taxable income for the tax year, gross income of $600 or more regardless of the amount of taxable income or a beneficiary who is a nonresident alien.