Are gift cards tax deductible IRS?

Emma Jordan

Published Feb 27, 2026

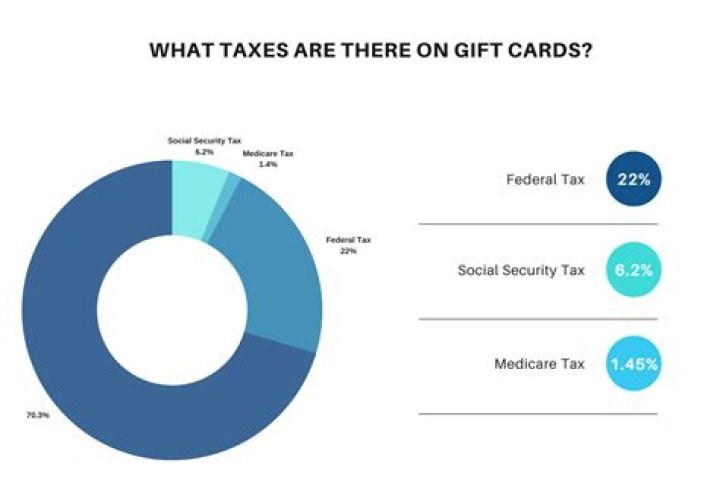

Gift cards and gift certificates are considered taxable income to employees because they can essentially be used like cash. The cost of the gift card is fully deductible to the business, but you must withhold taxes from the employee’s pay for these gifts.

Are gift card incentives taxable?

Yes, gift cards are taxable. According to the IRS, gift cards for employees are considered cash equivalent items. Like cash, you must include gift cards in an employee’s taxable income—regardless of how little the gift card value is.

Do you have to report a gift card to the IRS?

According to the IRS, since cash and cash-equivalent fringe benefits like gift certificates have a readily-ascertainable value, they do not constitute de minimis fringe benefits. This means that businesses must report gift cards as part of an employee’s wages on the Form W-2.

When to recognize gift card revenue for tax purposes?

The gift of complexity: Recognizing gift card revenue for tax purposes. Businesses often include gift card revenue in taxable income in the year the card is sold. This article discusses exceptions that permit deferral of that revenue for one or even up to two years. Gift cards have revolutionized our ability to purchase a last-minute gift.

Can a gift card be redeemed for non-integral services?

If the gift card can be redeemed for non-integral services, like third-party warranties or repair services, the revenue does not qualify for the two-year deferral. In December 2016, a customer purchases a $200 gift card from Electronic Store, Inc. which sells, delivers, and installs electronics.

What makes a gift certificate exempt from reporting?

A gift certificate, gift card, or in-store merchandise credit issued or maintained by any person engaged primarily in the business of selling tangible personal property at retail is exempt from reporting under this article.

Can a gift certificate with no expiration date be charged?

(e) A gift certificate or merchant stored value card which has no expiration date and does not impose a fee of any kind in relation to the sale, redemption or replacement of the certificate or card, other than an initial charge not exceeding the face value of the certificate or card, is exempt from the requirements of this section.