Are capital leases tax deductible?

Ava Robinson

Published Mar 30, 2026

A capital lease is treated like a loan, and the asset is considered owned by the lessee. The tax advantages of operating leases are especially significant for fixed assets such as lighting that are generally depreciated over a very long term (39 years), since the entire lease payment is tax deductible.

How do you determine if a lease is capital or operating for tax purposes?

If a lease does not meet the criteria of a capital lease then it is automatically treated as an operating lease. The payments from that lease are considered operating expenses and are recorded on the p&l when paid or incurred. The tax benefit of a capital lease often comes in the form of accelerated depreciation.

How are operating leases treated for income tax purposes?

For tax purposes, an operating lease will be treated as a true lease, with the lessor maintaining ownership of the asset and depreciation deductions, while the lessee has deductions related to rental payments. The lessor would recognize interest income in this situation.

What are the financial reporting differences between an operating lease and a capital lease?

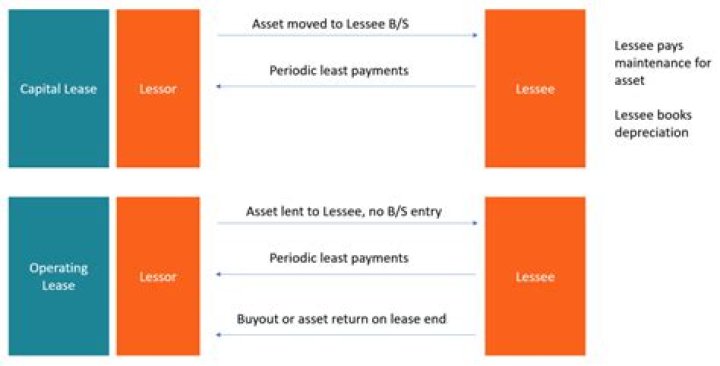

A capital lease (or finance lease) is treated like an asset on a company’s balance sheet, while an operating lease is an expense that remains off the balance sheet.

Can I depreciate a capital lease?

Because a capital lease is a financing arrangement, a company must break down its periodic lease payments into interest expense based on the company’s applicable interest rate and depreciation expense. A company must also depreciate the leased asset that factors in its salvage value and useful life.

Are operating leases fixed assets?

Accounting: Lease considered an asset (leased asset) and liability (lease payments). Payments are shown on the balance sheet. Tax: As owner, lessee claims depreciation expense, and interest expense.

What is the accounting for an operating lease?

The accounting for an operating lease assumes that the lessor owns the leased asset, and the lessee has obtained the use of the underlying asset only for a fixed period of time. Based on this ownership and usage pattern, we describe the accounting treatment of an operating lease by the lessee and lessor.