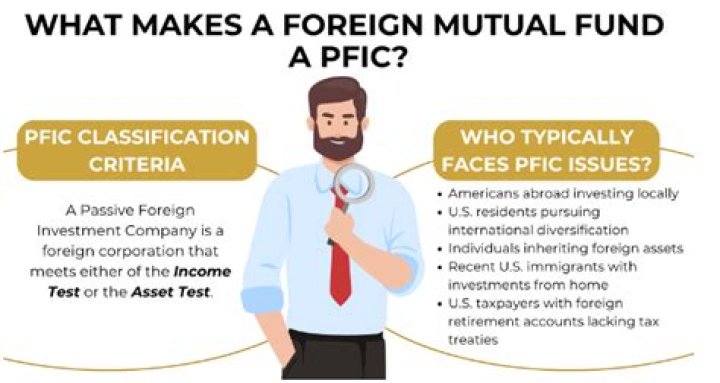

Are all foreign mutual funds PFIC?

Andrew Ramirez

Published May 13, 2026

The IRS strictly enforces PFIC Rules. Each of Your funds is considered to be a PFIC (Passive Foreign Investment Company). That is because the IRS hates Mutual Funds from overseas — so much so, that foreign mutual funds have been designated as PFICs for tax reporting purposes, which is very bad for tax purposes.

How do you determine if a mutual fund is a PFIC?

You can generally tell if a foreign corporation or foreign investment fund is considered a passive foreign investment company (PFIC) if it meets one of the following two characteristics: 75% or more of its gross income for the taxable year is passive income, or.

Are ETFs considered PFIC?

Canadian mutual fund trusts (including ETFs) and mutual fund corporations are considered PFICs and, therefore, are subject to the PFIC rules.

What percentage should you invest in international funds?

Most financial advisers recommend putting 15% to 25% of your money in foreign stocks, making 20% a good place to start. It’s meaningful enough to make a difference to your portfolio, but not too much to hurt you if foreign markets temporarily fall out of favor.

Are foreign stocks considered PFIC?

Stocks can be PFICs If the foreign corporation meets either the income test or the asset test, it is a PFIC. Most publicly traded stocks are not PFICs, because they are businesses producing primarily non-passive income and holding primarily non-passive assets.

What is passive income for PFIC?

A passive foreign investment company (PFIC) is a corporation, located abroad, which exhibits either one of two conditions, based on either income or assets: At least 75% of the corporation’s gross income is “passive”—that is, derived investments or other sources not related to regular business operations.

Who makes QEF election?

Any U.S. shareholder of a passive foreign investment company (PFIC) can elect to treat the PFIC as a qualified electing fund (QEF) and be taxed currently on a share of the QEF’s income (IRC § 1293 ).

How are foreign mutual funds taxed?

Though international mutual funds in India provide access to global equities, they are taxed like domestic debt or fixed income funds. Meanwhile, long-term capital gains attract a tax rate of 20% after providing the indexation benefit.

How do you determine if a company is a PFIC?

Under the income test, a foreign corporation is a PFIC if 75% or more of its gross income is passive income. Under the asset test, a foreign corporation is a PFIC if 50% or more of the average value of its assets consists of assets that would produce passive income.

Can a U.S. company be a PFIC?

If the corporation was treated as a PFIC in a closed year, it will continue to be treated as a PFIC. If the corporation ceases to be a PFIC under the new regulations, then the corporation is a “former PFIC” under Treas. Reg. Section 1.1291-9(j)(2)(iv).

How do I report foreign stocks?

Foreign stock or securities, if you hold them outside of a financial account, must be reported on Form 8938, provided the value of your specified foreign financial assets is greater than the reporting threshold that applies to you.

Is cash a passive asset for PFIC?

Notice 88-22 deemed all cash as a per se passive asset for PFIC-testing purposes; the proposed rule reflects the fact that some amount of cash is needed as working capital to support the day-to-day operations of an enterprise. Dividends from look-through subsidiaries.

What happens when you sell a PFIC?

All capital gains from the sale of PFIC shares are treated as ordinary income for federal income tax purposes and thus are not taxed at preferential long-term capital gain rates (Sec. 1291(a)(1)(B)).

What makes a PFIC a passive foreign investment company?

Passive Foreign Investment Company (“PFIC”) for US Investors A PFIC is defined as a foreign (non-US based) corporation that meets one of the following two tests: Income Test: 75% or more of its gross income is passive income (earnings derived from rental property, limited partnership or other enterprise not actively involved); or

When to include PFIC / QEF in Schedule K-1?

U.S. Treas. Reg. Section 1.1411-10 (g) Election with respect to CFC and PFIC/QEF income. The Schedule K-1 footnote disclosure will advise individual partner’s in the fund to make this election if the fund has included PFIC/QEF income in the partner’s Schedule K-1 taxable income.

Can a PFIC be treated as a qualified electing fund?

This regime applies when a shareholder elects to treat his or her PFIC investment as an investment in a qualified electing fund (QEF). It requires that PFIC shareholders be taxed on undistributed PFIC income as it is earned. Interest on tax deferral (IRC section 1291).

How to determine if a company is a PFIC?

There are two main tests to determine if a person has a PFIC. There is the Asset Test and the Income Test. As provided by the IRS: “A foreign corporation is a PFIC if it meets either the income or asset test described next. Income Test. 75% or more of the corporation’s gross income for its tax year is passive income (as defined in section 1297(b)).